Become a PowerPoint Guru by Dave Tracy

Become a PowerPoint Guru by Dave Tracy

Learn the methodologies, frameworks, and tricks used by Management Consultants to create executive presentations in the business world.

Become a PowerPoint Guru by Dave Tracy

A commonly quoted statistic is that 80% to 95% of the cost of a product is determined by its design and is therefore set before the item enters manufacturing. This  assumption suggests that the dominant focus of Cost Management should be during Product Development and not during Manufacturing.

assumption suggests that the dominant focus of Cost Management should be during Product Development and not during Manufacturing.

However, contrary to a widely held assumption, companies can integrate a variety of Cost Management techniques not only in the design phase but throughout the product life cycle. This is to ensure that there is a substantial reduction in costs. In fact, companies achieving Operational Excellence and competing aggressively on cost might consider the adoption of some form of an Integrated Cost Management Program that spans the entire product life cycle.

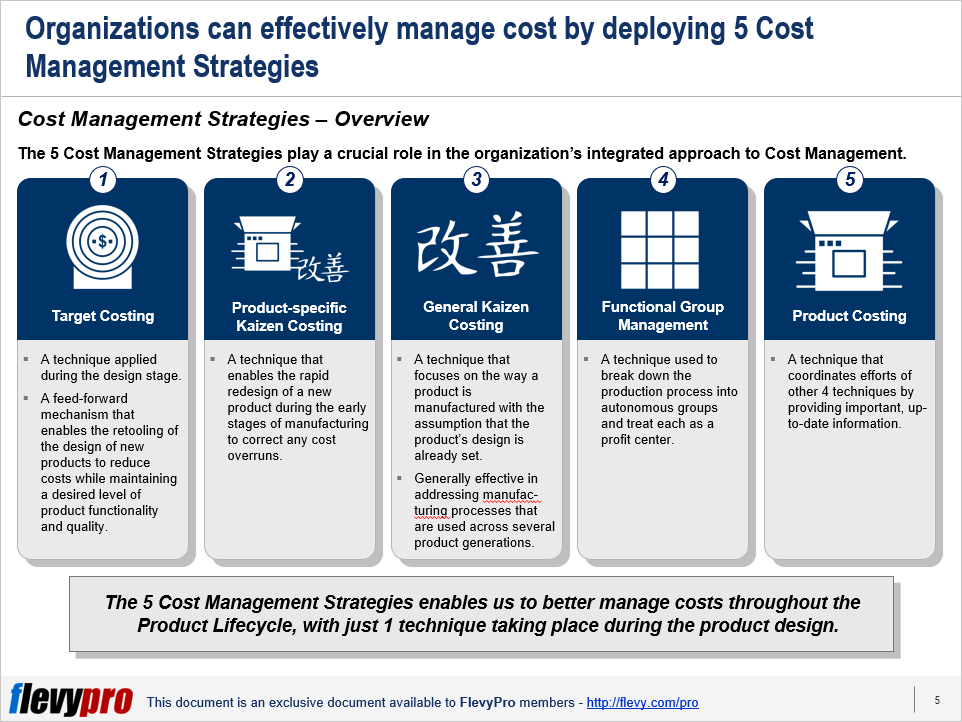

An organization must have a good understanding of Integrated Cost Management and the 5 Cost Management Strategies that they can use to reduce costs but still attain the desired level of functionality and quality at the target costs.

The 5 Cost Management Strategies play a crucial role in the company’s integrated approach to Cost Management.

The 5 Cost Management Strategies can be applied throughout the product life cycle with one technique used during the product design and the rest during manufacturing.

Kaizen Costing as known as continuous improvement costing. It is a method of reducing managing costs. Kaizen Costing has a similarity with Target Costing but it also has its differences. (Note: Kaizen is the Japanese term for Continuous Improvement and often tied to the philosophy of Lean Management.)

Both Kaizen Costing and Target Costing can achieve results with lower resources. This is basically their similarity. On the other hand, the differences lie in their usage and involvement.

Target Costing is used on the design stage and requires the involvement only of designers. On the other hand, Kaizen Costing is used during the manufacturing stage and requires high involvement of employees. The general idea of Kaizen Costing is to determine target costs, design products, and process to not exceed those costs.

Interested in gaining more understanding of these Cost Management Strategies? You can learn more and download an editable PowerPoint about 5 Cost Management Strategies here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

There is a general belief among organizations that a large percentage of a product’s costs are locked in by design. It is assumed that little can be done once the  design is set. This assumption has influenced cost management programs across diverse products’ life cycles. As a result, the focus during the design phase is Cost Reduction and Cost Containment during the manufacturing phase.

design is set. This assumption has influenced cost management programs across diverse products’ life cycles. As a result, the focus during the design phase is Cost Reduction and Cost Containment during the manufacturing phase.

Yet, organizations that operated in a highly competitive market and demanded aggressive cost management showed that costs can be aggressively managed throughout the product life cycle. Various cost management strategies or techniques may be used to increase the program’s overall effectiveness. One of them is the Integrated Cost Management.

Integrated Cost Management is every organization’s prescription for lower cost and higher profits. It is the 21st business approach to achieving Cost Management efficiency.

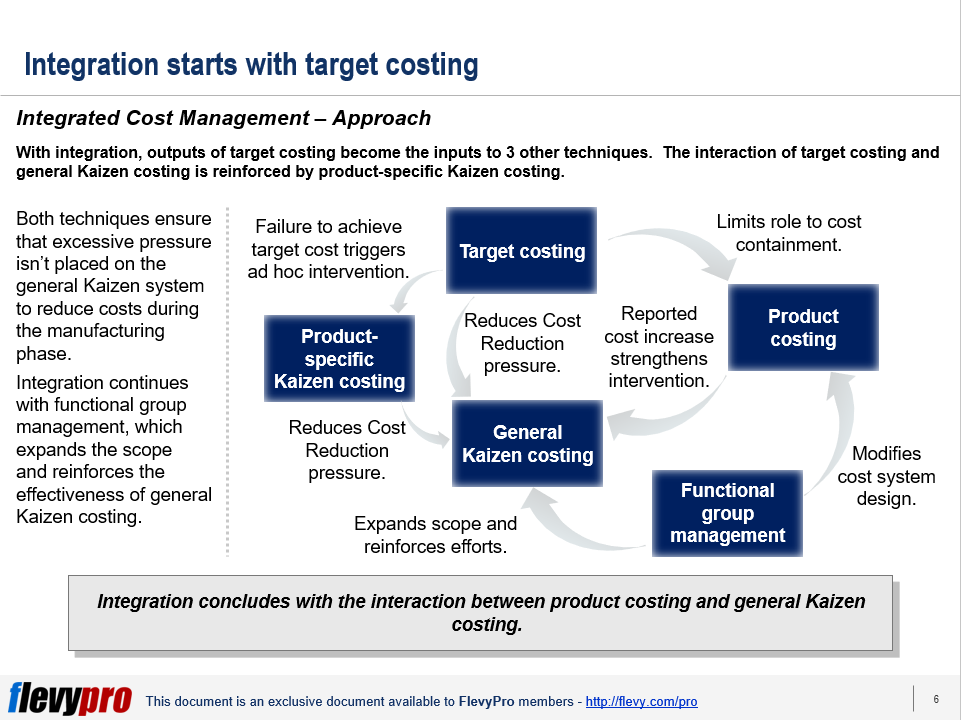

Integration is necessary for Strategy Development as it can promote the achievement of the company’s profit objectives. In fact, there are major benefits to Integrated Cost Management. One of which is lowering of overall costs throughout the product life cycle.

Integrated Cost Management can facilitate a steady decrease in costs all the way to discontinuance. In fact, it can result in an annual cost reduction of about 17% during manufacturing, savings that exceed 30$%, and a designed-in cost of below 70%.

Achieving this requires an understanding of the Integrated Cost Management Approach.

The Integrated Cost Management Approach focuses on the integration of cost management techniques which can lead to higher levels of cost reduction and superior overall performance.

The Integrated Cost Management Approach takes into consideration 5 Cost Management Strategies.

The 5 Cost Management Strategies enable organizations to better manage costs throughout the product life cycle, with just one (1) technique taking place during the product design and the rest during manufacturing.

The application of the 5 Cost Management strategies has its key takeaways. These can be used as a guidepost in its application and a model of general concepts that organizations may consider.

One key takeaway is significant savings can still be achieved with short life cycle products and aggressive cost management focused on product design. Taking to note this key takeaway, we have to consider that as the length of the manufacturing phase of the product’s life cycle increases, the opportunity for cost reduction increases. Further, there is a need to explore the value of integrating multiple cost management during manufacturing.

Interested in gaining more understanding of Integrated Cost Management? You can learn more and download an editable PowerPoint about Integrated Cost Management here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.