Become a PowerPoint Guru by Dave Tracy

Become a PowerPoint Guru by Dave Tracy

Learn the methodologies, frameworks, and tricks used by Management Consultants to create executive presentations in the business world.

Become a PowerPoint Guru by Dave Tracy

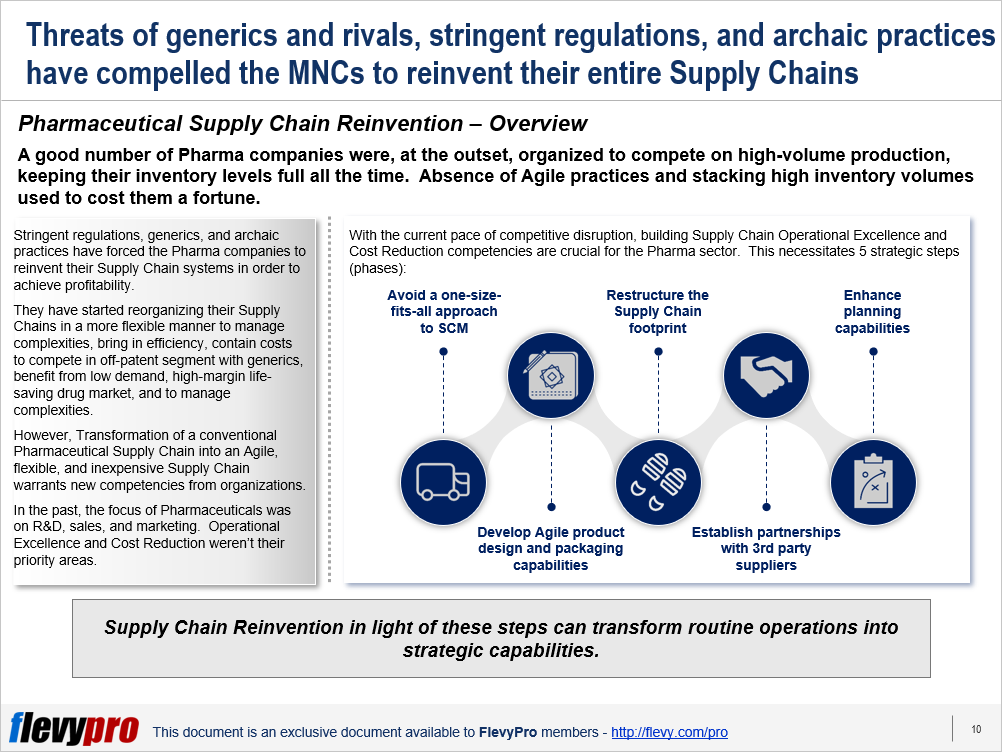

Majority of pharmaceutical companies are persisting with decade old processes and routines. They have transactional relationships with suppliers, lack of concerted efforts to progress ahead, and no vision to reap productivity rewards. The reasons for continuing with these traditional practices include tax regimes, regulatory hurdles, and stable revenues from customers dependent on existing industry offerings.

Majority of pharmaceutical companies are persisting with decade old processes and routines. They have transactional relationships with suppliers, lack of concerted efforts to progress ahead, and no vision to reap productivity rewards. The reasons for continuing with these traditional practices include tax regimes, regulatory hurdles, and stable revenues from customers dependent on existing industry offerings.

Disruption—spurred by technological Innovation, fluctuating customer demand patterns, and more agile and creative competitors—has forced the pharmaceutical sector to think of ways to face these challenges, survive, and thrive. One of the strategic response to this competitive disruption—by leading manufacturers—is to reexamine their manufacturing operations, embracing agile principles, reducing costs, revolutionizing procurement and distribution functions, and striving to achieve Operational Excellence. Above all, they view their supply chain not as a cost center, but as a source of Competitive Advantage.

The increasing influence of generic drugs is another challenge for large multinational pharmaceuticals. In the past, multinational companies (MNCs) dominated the market owing to possessing a number of high-market drugs protected under patents. Patent protection afforded them the leverage to set high prices on each product. The scenario is fast changing. Expiry of high-market drugs patents is creating a huge opening for generic competitors and the space is widening compared to the past.

In the past, pharma manufacturers were able to counter the threat to generic competitors by developing new drugs. However, this is becoming difficult and the new drugs pipeline is shrinking with time. R&D expenditure has continuously gone up, however, drug approval from the authorities has not kept paced with it. It has rather declined, straining the MNCs further.

Other disruptive factors include newer distribution methods, public health plans favoring generic drugs over proprietary ones due to cost effectiveness, the newer internet / mail delivery options displacing traditional pharmacy dispensing options. Pharmacy chains—e.g. Walgreens—have given a leverage to the retailers to negotiate reduction in medicine prices where again generics have an edge over MNCs.

Moreover, the trend of drugs purchased through a formal tender process is increasingly gaining acceptance, adding to the difficulties of large pharma manufacturers. Additionally, strict regulations are minimizing the cost benefits that MNCs traditionally enjoyed in the past.

All these factors have forced the pharma companies to reorganize their Supply Chains in a more flexible manner to manage complexities, bring in efficiency, and contain costs to compete in off-patent segment with generics.

Reorganization of a conventional pharmaceutical Supply Chain into an Agile, flexible, and inexpensive Supply Chain warrants developing Operational Excellence and Cost Reduction competencies. This necessitates 5 strategic steps (phases):

Let’s discuss these steps in detail.

Large pharma MNCs typically maintain the Supply Chain of all of their drugs with a single strategy of retaining high inventory and service levels. Such a strategy can only work for products having a high profit margin, in a static environment. It is not suitable for low-margin products, contrasting environments, and does not take into account fluctuations in demand patterns. An appropriate approach is to implement a multiple Supply Chains model based on individual products and markets.

The 2nd step in Pharma Supply Chain Reinvention involves quick distribution of different versions of products to markets based on demand. For low-margin products with high demand volatility, the Supply Chain Management Strategy should be to employ Pack-to-Order system. The Pack-to-Order approach involves developing a version of a product that could be timely dispatched to several markets of varying demand across the globe. This approach coupled with Postponement Strategy—where products are packed to order during later stages of production based on regional demand—assists in trimming down the inventory, reducing complicatedness, and enhancing Supply Chain nimbleness to demand volatility.

Interested in learning more about how to reinvent your Pharmaceutical Supply Chain? You can download an editable PowerPoint on Pharmaceutical Supply Chain Reinvention here on the Flevy documents marketplace.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Early 2000s saw a change of mind regarding the Globalization of commerce by members of the political and economic arenas. This change of mind was instigated by myths perpetuated against commerce Globalization because of the dichotomy that appeared between existing Operating Models of companies and needs of the emerging markets.

These perceived trade-offs that were myths included ideas like choosing between centrally-controlled Operating Model and local responsiveness model.

Proponents of the central model had the view that intellectual power and Innovation capability had to be centralized, all products and services brought in line everywhere, foregoing catering to diverse needs and demands of customers in every emerging market.

The converse view was that in order to have locally applicable distribution systems, proactive Supply Chains, and reduced costs of emerging-market management, it was necessary to devolve the company and operation as a loose federation.

This trade-off incompatibility was addressed by the Hub Strategy where, in place of a single center, companies set up principal office “hubs” in as many of the 20 gateway countries of the world as required—a global corporate structure with no headquarters.

These 20 gateway countries represent 70% of the world population and generate 80% of the world income. The gateway countries include Australia, Canada, France, Germany, Italy, Japan, the Netherlands, Spain, the United Kingdom, and the United States from the developed economies. Rest of the 10 are emerging markets of Brazil, China, India, Indonesia, Mexico, Russia, South Africa, South Korea, Thailand, and Turkey.

This new Business Model covers both the recognized advantages of developed markets and the possibilities of emerging economies. A model that handles decentralization, centralization, existing practices, and possible disruptions not as trade-offs, but as complements.

It is, however, important to understand that for the model to have its full impact, 3 core pillars have to be integrated and pursued simultaneously. The 3 Pillars of Globalization are:

Only business leadership that has taught itself and its teams to be very careful about where to customize, how to develop capabilities, and what to arbitrage are the ones reaping benefits from this model.

Let us delve a little deeper into the details of the 3-pillar Business Model.

Variation in needs, wants, and cultures of consumers makes it impossible to customize centrally. Providing products and services in a locally competitive manner is therefore central to become a global enterprise.

Customization entails fulfilling the requirements and wants of varied consumers, in areas such as product or service features, affordability, and cultural alignment. Hub Strategy provides the leverage to fulfill this demand by enabling companies to customize only in the 20 gateway countries.

Unity entails worldwide alignment of the company with, a unified central purpose, a body of exclusive first-rate knowledge, and capabilities that differentiate the company from all others.

Core purpose must be understood in the same manner by all functions of the company, in every geographical location.

Arbitrage is a methodical initiative that consists of increasing effectiveness and Cost Reduction by discovering materials, manufacturing methods, logistics practices, funds sourcing, or infrastructure that are less expensive.

Interested in learning more about the 3 Pillars of Globalization and its Case examples? You can download an editable PowerPoint on 3 Pillars of Globalization here on the Flevy documents marketplace.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

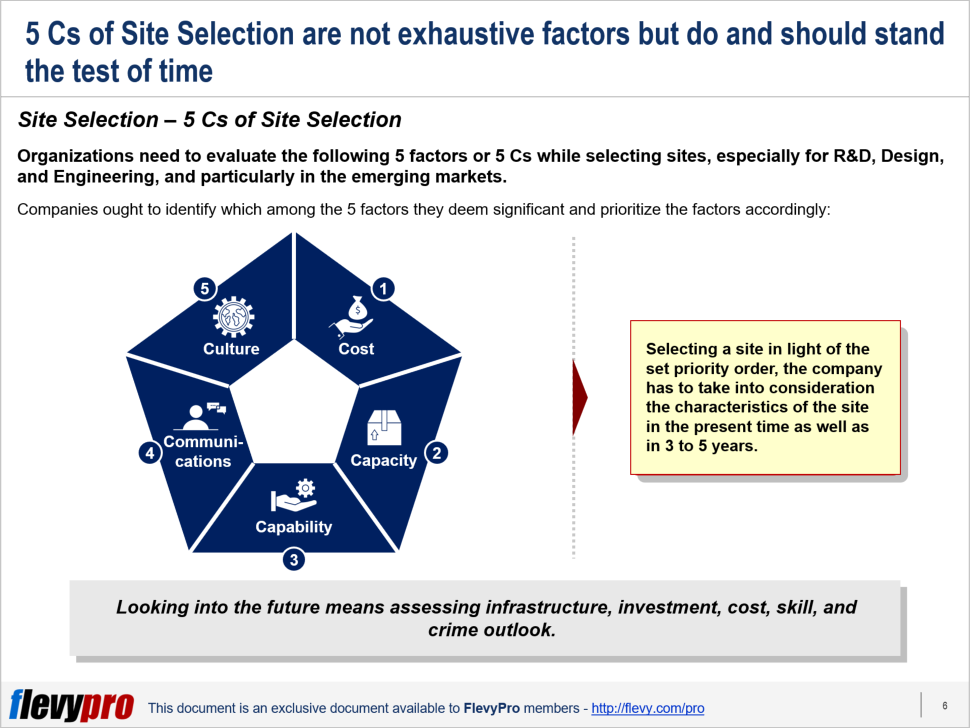

Site Selection is the practice of choosing a new facility location. It involves measuring the needs of a new project against the merits of potential locations. The practice became popular during the 20th century, as operations of many organizations expanded to new geographies on a national and international scale.

Selection of sites has been known to have taken place due to factors such as:

Making such significant long-term choices based on haphazard and indifferent reasons is a blunder. The consequences of the mistake are exacerbated when such sites are being selected in emerging markets.

Site selection, in particular, for R&D, Design, and Engineering, warrants a more serious approach than is given to it. Employing a formalized selection method aids in eliminating sentiment in the concluding decision. The orderly selection procedure is also valuable in conveying the ultimate decision to all involved. Selection criteria and their priority should be agreed to in advance for removal of any partiality from the Site Selection process.

Site Selection, especially when being done in emerging markets, has to be conducted while considering at least 5 factors—or the 5 Cs of Site Selection. Companies ought to identify which among the 5 factors they deem significant and prioritize the factors accordingly:

Selecting a site in light of the set priority order, the company has to take into consideration the characteristics of the site in the present time as well as in 3 to 5 years.

Let us delve a little deeper into some of the factors.

Ideally, Cost Reduction should not be the only factor influencing site selection decisions. If Cost factor is predominant in the decision, then the local standard of living and the changes there to, have to be taken into consideration. Costs in setting up a site include items such as:

Companies basing their decisions exclusively on Cost factor rather than what suits their requirements end up paying more than estimated.

Capability is the ability of the site under consideration to provide the necessary infrastructure, resources, and the work/ operational environment required by the company. Capability includes existence of exclusive skills and expertise that a company explicitly needs.

Also advantageous to capability are nearby R&D, design, testing, and prototyping centers setup by foreign and local companies.

Capacity refers to the abundance of qualified skill available on the site under consideration. Capacity comes into play when the company needs rapid scaling up of its operations.

Although the 5 Cs are of extreme significance, there is an additional factor that cannot be ignored—the Customer. Recent advances in technology and communication have further empowered the Customer. The result is that more organizations are seeking to focus on Customer-centric Design.

Interested in learning more about 5 Cs of Site Selection? You can download an editable PowerPoint on 5 Cs of Site Selection here on the Flevy documents marketplace.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

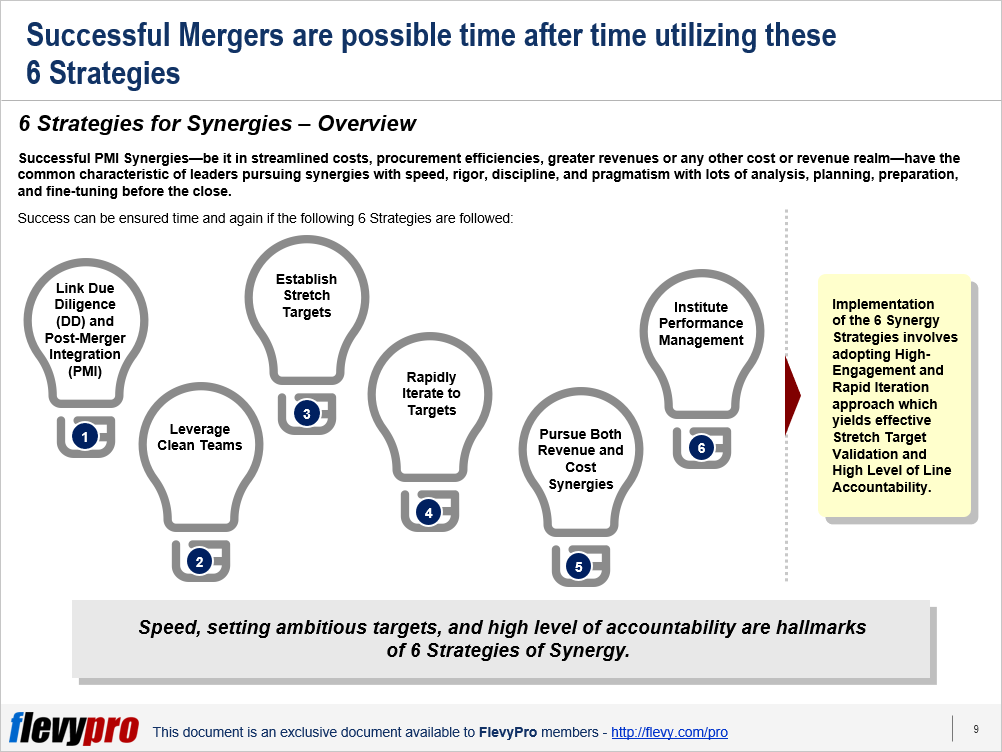

A significant number of Mergers remain unsuccessful, because companies do not employ a thorough and disciplined approach to realizing Post-Merger Integration Synergies. In reasons for failure, we hear remarks like:

A disciplined and rational approach to pursuing Merger Synergies is key to successful Post-Merger Integration (PMI). Companies that authenticate and set pragmatic yet ambitious Post-Merger Integration Synergy targets do the following to exceed targets and achieve substantial share price premium and a significant Competitive Advantage:

Successful PMI Synergies—be it in Cost Optimization, Strategic Sourcing, Greater Revenues or any other Cost or Revenue realm—have the common characteristic of leaders pursuing synergies with speed, rigor, discipline, and pragmatism with lots of analysis, planning, preparation, and fine-tuning before the close.

Success can be ensured time and again if the 6 Strategies for Post-Merger Integration Synergies are followed to the letter:

Implementation of the 6 Synergy Strategies involves adopting High-Engagement and Rapid Iteration approach which yields effective Stretch Target Validation and High Level of Line Accountability.

Let us delve a little deeper into 2 of these PMI Synergy Strategies.

Linking DD to PMI ensures realistic estimates on part of the DD team thus avoiding formulation of broad-brushed and imprecise Synergies. Linking also guarantees greater amount of ownership and accountability at the same time enabling more compelling Stretch Targets. Linking of DD to PMI is necessary because:

Successful Mergers ensure a harmonized hand-off from Due Diligence teams to Integration Planning teams by ensuring the following:

Clean team is an independent group that is tasked with the collection and analysis of sensitive company data—pre-closure—with the guidance of management. Clean team may comprise of third-party members or employees who can be reassigned out of business in case of deal failure eradicating the risk of compromising confidential information. Clean team is formed by legal contract based on protocols agreed to by both company’s legal departments. Clean teams help by:

Interested in learning more about the 6 Strategies for Post-Merger Integration Synergies? You can download an editable PowerPoint on Post-Merger Integration (PMI): 6 Strategies for Synergies here on the Flevy documents marketplace.

Gain the knowledge and develop the expertise to become an expert in Post-merger Integration (PMI). Our frameworks are based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. Click here for full details.

M&A is an extremely common strategy for growth. M&A transactions always look great on paper. This is why the buyer typically pays a 10-35% premium over the of the target company’s market value.

However, when it comes time for the Post-merger Integration (PMI), are we really able to capture the expected value? Studies show only 20% of organizations capture projected revenue synergies and only 40% capture cost synergies. Not to mention, the PMI process is typically very painful, drawn out, and politically charged, often resulting in the loss of key personnel.

Learn about our Post-merger Integration (PMI) Best Practice Frameworks here.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Cut-throat competition in industries has driven companies to find ways to reduce costs while increasing efficiency. To accomplish this, most companies have skillfully endeavored to streamline Sales, Operations Planning, Forecasting, Inventory Management, and Logistics.

One area that has still not grabbed industry’s attention is out-bound Supply Chain Management–from packaging to final delivery. Companies generally neglect Supply Chain simply because they do not consider it their core competency.

Significant Cost Reduction in the Supply Chain can be achieved by focusing on 2 main cost categories:

Warehousing and Transportation represent a significant portion of the total Logistics costs. Implementing improvement programs, without any significant capital investments, can enable 20-50% cost saving in Warehousing, 40% in Transportation costs, flexibility, and better service.

Supply Chain Cost Reduction in Transportation and Warehousing has vast potential, not only in terms of costs, but also Process Improvement using Lean Six Sigma (LSS) techniques.

The approach to Supply Chain Cost Reduction in Warehousing encompasses 3 phases:

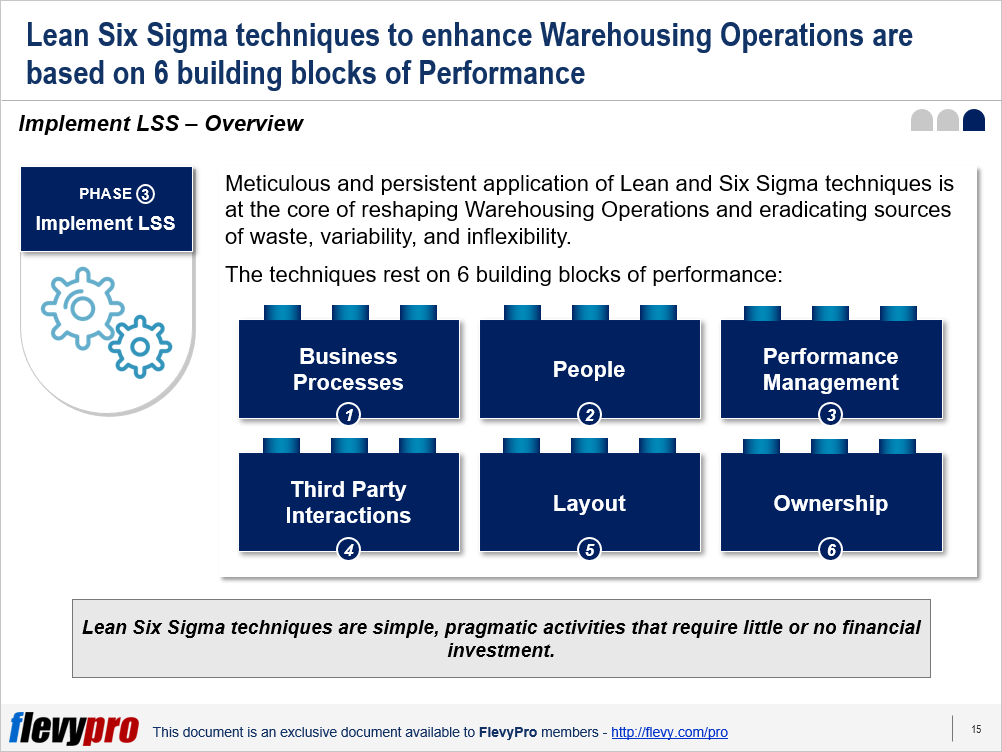

Meticulous and persistent application of Lean Management and Six Sigma techniques is at the core of reshaping Warehousing Operations and eradicating sources of waste, variability, and inflexibility. This article is an overview of the 6 building blocks used in Implementing Lean Six Sigma (LSS)—the 3rd phase of the approach to Supply Chain Cost Reduction in Warehousing:

Let us dive a little deeper into some of the building blocks.

Business Processes present a huge opportunity for improvement by eliminating redundancies and sources of waste in Warehouse operations (e.g., unnecessary motion or double-handling in Manufacturing). Each source of waste represents extra costs and inflexibility that can be reduced or eliminated.

Business Process Improvement can help reduce:

This building block of Implementing Lean Six Sigma aims at avoiding overstaffing of full-time employees and at the same time maintaining a well-trained, efficient workforce.

Streamlining this building block leverages the following benefits to organizations:

This building block aims at using existing Performance Management levers to improve Employee Performance through morale boosting and awareness exercises. A laser-focus on the performance element helps the leadership achieve the following benefits:

Given the existing industry cost and performance demands, wasteful or unpredictable Warehouse operations lose more than money. This can do rapid and permanent harm to a company’s reputation with customers since distribution is the logistical interface with the customer.

Improving Warehouse Operations is a significant area not only for Cost Reduction, but also a source of refining Customer Value Proposition.

Interested in learning more about Supply Chain Cost Reduction in Warehousing and Lean Six Sigma? You can download an editable PowerPoint on Supply Chain Cost Reduction: Warehousing here on the Flevy documents marketplace.

Gain the knowledge and develop the expertise to become an expert in Supply Chain Management (SCM). Our frameworks are based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. Click here for full details.

Supply Chain Management (SCM) is the design, planning, execution, control, and monitoring of Supply Chain activities. It also captures the management of the flow of goods and services.

In February of 2020, COVID-19 disrupted—and in many cases halted—global Supply Chains, revealing just how fragile they have become. By April, many countries experienced declines of over 40% in domestic and international trade.

COVID-19 has likewise changed how Supply Chain Executives approach and think about SCM. In the pre-COVID-19 era of globalization, the objective was to be Lean and Cost-effective. In the post-COVID-19 world, companies must now focus on making their Supply Chains Resilient, Agile, and Smart. Additional trends include Digitization, Sustainability, and Manufacturing Reshoring.

Learn about our Supply Chain Management (SCM) Best Practice Frameworks here.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Reorganization becomes essential at some stage in the lifecycle of any organization. In order to emerge triumphant through this tumultuous challenge, it is necessary that the focus remains on the challenges impeding the organization, thorough Strategic Planning to tackle the challenges, and prioritizing strategic initiatives to deliver effective Business Transformation. Strategic Restructuring has the capability to deliver these results.

When the word “Restructuring” pops up, the foremost idea that comes to mind is achieving Cost Reduction by minimizing payroll costs—predominantly by cutting back on the headcount.

Scores of organizations have suffered because, in the melee of headcount reduction, the most competent employees quickly found opportunities elsewhere, leaving inappropriately competent employees behind, resulting in a crippled organization.

The purpose of Restructuring is to make the organization profitable, efficient, and effective. Headcount reduction should be a consequence of the Restructuring initiative and not the prime objective.

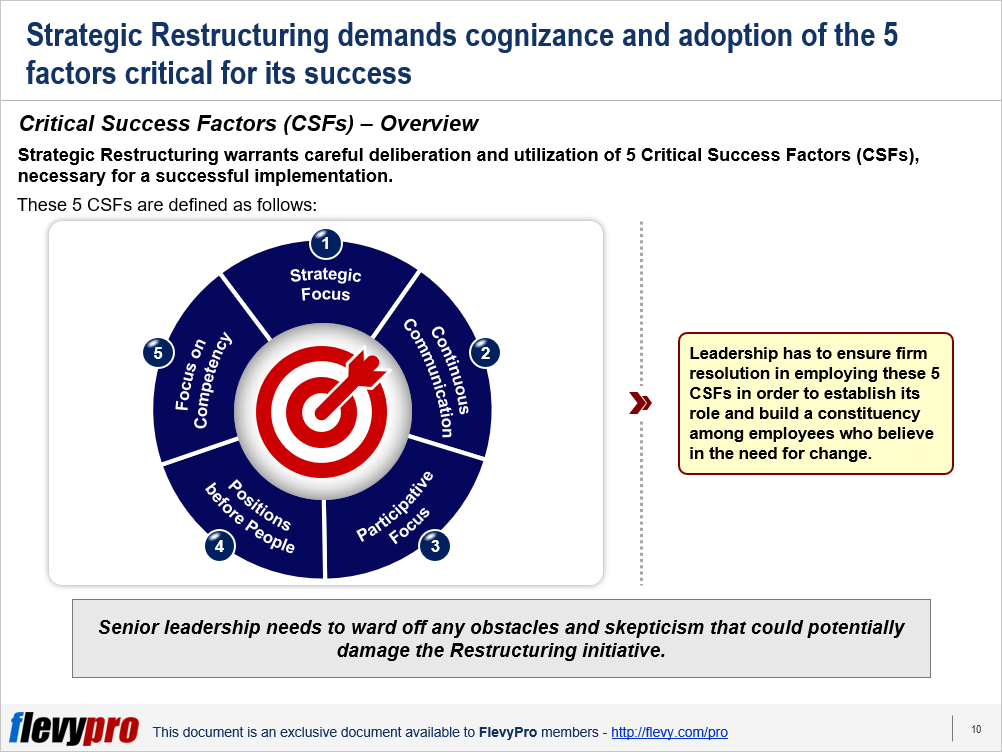

To avoid an outcome that debilitates the organization as a result of Restructuring, it is absolutely essential to keep an eye on the Critical Success Factors (CSFs) while the organization moves through the 4 phases of Strategic Restructuring. Strategic Restructuring’s 5 CSFs include:

Experts suggest envisioning a “Future State” for the organization, to be achieved through a robust Strategy that includes Change Management, implemented by the most competent employees who are redeployed. The rest of the employees either severe ties voluntarily or are laid off—ideally with a good severance package or a job placement, with the organization’s help, somewhere else.

Leadership has to ensure firm resolution in employing these Critical Success Factors in order to establish its role and build a constituency among employees who believe in the need for change. Let’s dig deeper into the 5 CSFs of Strategic Restructuring.

Interested in learning more about the Restructuring’s Critical Success Factors, Transformation Phases, and a Case Study on Restructuring?” You can download an editable PowerPoint on Strategic Restructuring: Critical Success Factors on the Flevy documents marketplace.

Gain the knowledge and develop the expertise to become an expert in Business Transformation. Our frameworks are based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. Click here for full details.

“If you don’t transform your company, you’re stuck.” – Ursula Burns, Chairperson and CEO of VEON; former Chairperson and CEO of Xerox

Business Transformation is the process of fundamentally changing the systems, processes, people, and technology across an entire organization, business unit, or corporate function with the intention of achieving significant improvements in Revenue Growth, Cost Reduction, and/or Customer Satisfaction.

Transformation is pervasive across industries, particularly during times of disruption, as we are witnessing now as a result of COVID-19. However, despite how common these large scale efforts are, research shows that about 75% of these initiatives fail.

Leverage our frameworks to increase your chances of a successful Transformation by following best practices and avoiding failure-causing “Transformation Traps.”

Learn about our Business Transformation Best Practice Frameworks here.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

![]() Companies looking to improve efficiency and reduce costs can gain significant ground in the Supply Chain Management function by incorporating Lean Management and Six Sigma techniques.

Companies looking to improve efficiency and reduce costs can gain significant ground in the Supply Chain Management function by incorporating Lean Management and Six Sigma techniques.

Reason this area has gone under the radar is that companies do not consider Supply Chain to be their core competency.

Not only Warehousing but Transportation also has almost the same potential in terms of opportunities for Cost Reduction and Process Improvement. The approach to Transportation Costs Reduction, though, is different to that of Supply Chain Cost Reduction in Warehousing. This is in part due to the complexity in Transportation Costs, as the costs come from numerous widely distributed individual operations every year.

The approach to Supply Chain Cost Reduction in Transportation encompasses 2 phases:

![]()

Let us delve a little deeper into the 2 phases.

Improvement in Transportation operations is hindered, in most cases, by enormous variability in operations, diverse service levels being demanded by various customers, and a multitude of transport providers delivering services in a variety of ways.

Transportation Costs of between 20-30% can be saved by compiling a complete perspective of the overall Transportation operations of an organization. The evaluation will also reveal essential service categories that have a skewed effect on Cost.

Identification of the Cost Drivers is imperative for the companies to develop a systematic approach to Transportation Cost Reduction. This systematic approach involves observing 4 main levers of Cost Optimization opportunities:

The 4 levers of Cost Reductions help in countering the issues impacting Transportation Costs and enabling significant savings.

Significant Cost Reductions can be gained by identifying mutual benefits and risks for both companies and suppliers in addition to understanding customer breakpoints that enable Customer Centric Design.

Let us consider a few instances where Cost Reduction can have a quick impact.

Interested in learning more about the phases and cost drivers of Supply Chain Cost Reduction in Transportation? You can download an editable PowerPoint on Supply Chain Cost Reduction: Transportation here on the Flevy documents marketplace.

Gain the knowledge and develop the expertise to become an expert in Supply Chain Management (SCM). Our frameworks are based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. Click here for full details.

Supply Chain Management (SCM) is the design, planning, execution, control, and monitoring of Supply Chain activities. It also captures the management of the flow of goods and services.

In February of 2020, COVID-19 disrupted—and in many cases halted—global Supply Chains, revealing just how fragile they have become. By April, many countries experienced declines of over 40% in domestic and international trade.

COVID-19 has likewise changed how Supply Chain Executives approach and think about SCM. In the pre-COVID-19 era of globalization, the objective was to be Lean and Cost-effective. In the post-COVID-19 world, companies must now focus on making their Supply Chains Resilient, Agile, and Smart. Additional trends include Digitization, Sustainability, and Manufacturing Reshoring.

Learn about our Supply Chain Management (SCM) Best Practice Frameworks here.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Organizations that have survived over time have had to reinvent themselves over and over with the changes in the environment. These Business Transformations almost always include Cost Reduction that tend to lean towards Headcount Reduction. Headcount Reduction is typically achieved using 2 approaches:

Organizations that have survived over time have had to reinvent themselves over and over with the changes in the environment. These Business Transformations almost always include Cost Reduction that tend to lean towards Headcount Reduction. Headcount Reduction is typically achieved using 2 approaches:

Downsizing keeps the fundamentals of the roles same with only fewer people performing those roles. Whereas, Restructuring creates new roles, as well as modify existing roles, requiring a new mix of skills or altogether new resources to perform them.

Restructuring presents a more challenging task in that a new mix of skills has to be identified for each role, an Assessment Process has to be set up to assess existing employees against new competencies, and Redeployment after Restructuring (or new recruitment) done.

The important question in both scenarios is: Who should we eliminate and who should stay?

The question can be answered by devising and using key criteria to evaluate and then choose the most relevant assessment method.

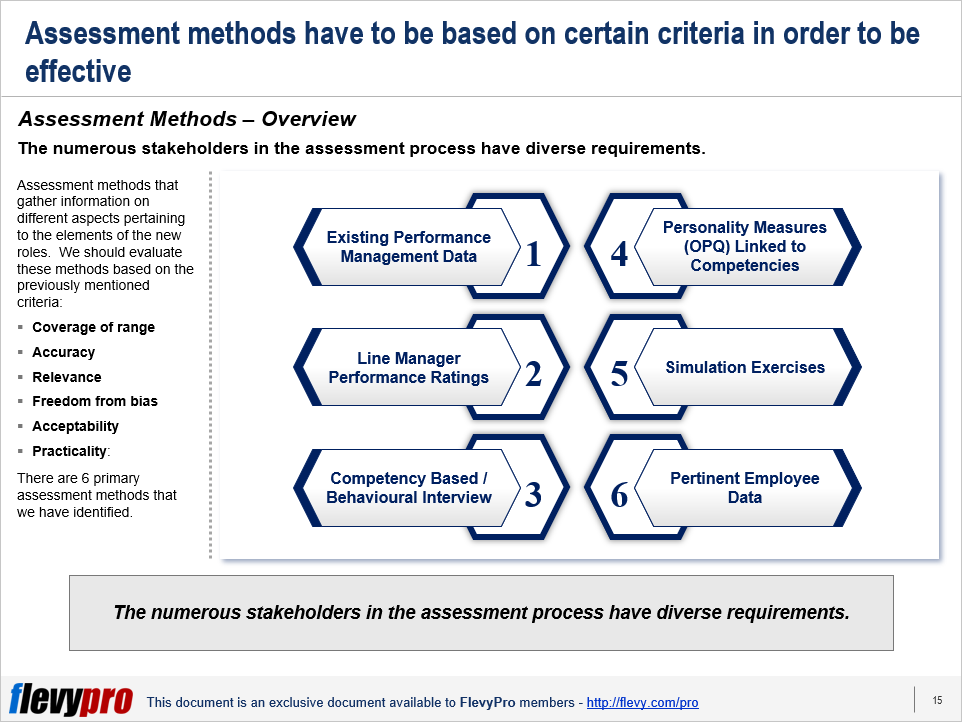

Assessment of employees is key in both Downsizing as well as Restructuring. The Assessment Process has to be vigorous enough to identify the right employees to keep and lay off. A broader assessment process ensures coverage of more aspects of a new role which in turn makes the assessment process fairer. Measures, in this regard, may include:

Linkage of the entire assessment process to the requirements of the job is the crucial part of this phase.

As with any assessment system, the content and design will be settled through consideration of various factors, some practical like cost, logistics and some more about safeguarding the output like instrument validity. When taking into account assessment tools for incorporation in the process it is beneficial to examine them against following criteria:

The tools, based on the above criteria, help in various assessment methods that gather information on different aspects pertaining to the elements of the new roles. The most widely used Assessment methods include:

Let us examine the methods in a little more detail.

There are various benefits of using this employee assessment method, such as:

There are some drawbacks associated with the existing Performance Management data method that executives should be mindful of:

Such data although convenient and easy to obtain, has to be augmented from other sources—and through other assessment methods—for a complete picture to base the employee selection decision on.

Interested in learning more about Redeployment Assessment Process & Methods? You can download an editable PowerPoint on Restructuring: Redeployment Assessment Process & Methods here on the Flevy documents marketplace.

Gain the knowledge and develop the expertise to become an expert in Business Transformation. Our frameworks are based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. Click here for full details.

“If you don’t transform your company, you’re stuck.” – Ursula Burns, Chairperson and CEO of VEON; former Chairperson and CEO of Xerox

Business Transformation is the process of fundamentally changing the systems, processes, people, and technology across an entire organization, business unit, or corporate function with the intention of achieving significant improvements in Revenue Growth, Cost Reduction, and/or Customer Satisfaction.

Transformation is pervasive across industries, particularly during times of disruption, as we are witnessing now as a result of COVID-19. However, despite how common these large scale efforts are, research shows that about 75% of these initiatives fail.

Leverage our frameworks to increase your chances of a successful Transformation by following best practices and avoiding failure-causing “Transformation Traps.”

Learn about our Business Transformation Best Practice Frameworks here.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of Target Costing. Target Costing is referred to as an organized process to determine the cost at which a proposed product must be developed so as to generate profits at the product’s anticipated selling price in future.

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of Target Costing. Target Costing is referred to as an organized process to determine the cost at which a proposed product must be developed so as to generate profits at the product’s anticipated selling price in future.

In highly competitive markets such as FMCG, construction, healthcare, and energy, prices are determined by market forces. Producers cannot effectively control selling prices. The only control, to some extent, is over costs, so management’s focus has to be on influencing every component of product, service, or operational costs.

Target Costing is a proactive Cost Planning, Cost Management, and Cost Reduction practice. Costs are planned and managed out of a product and business early in product life-cycle, rather than during the later stages. The fundamental objective of Target Costing is to make the business profitable in any competitive marketplace. Target Costing is widely used in several industries e.g. manufacturing, energy, healthcare, construction, and a host of others.

Some key features of Target Costing are:

Target Costing presents the following advantages over other product pricing techniques:

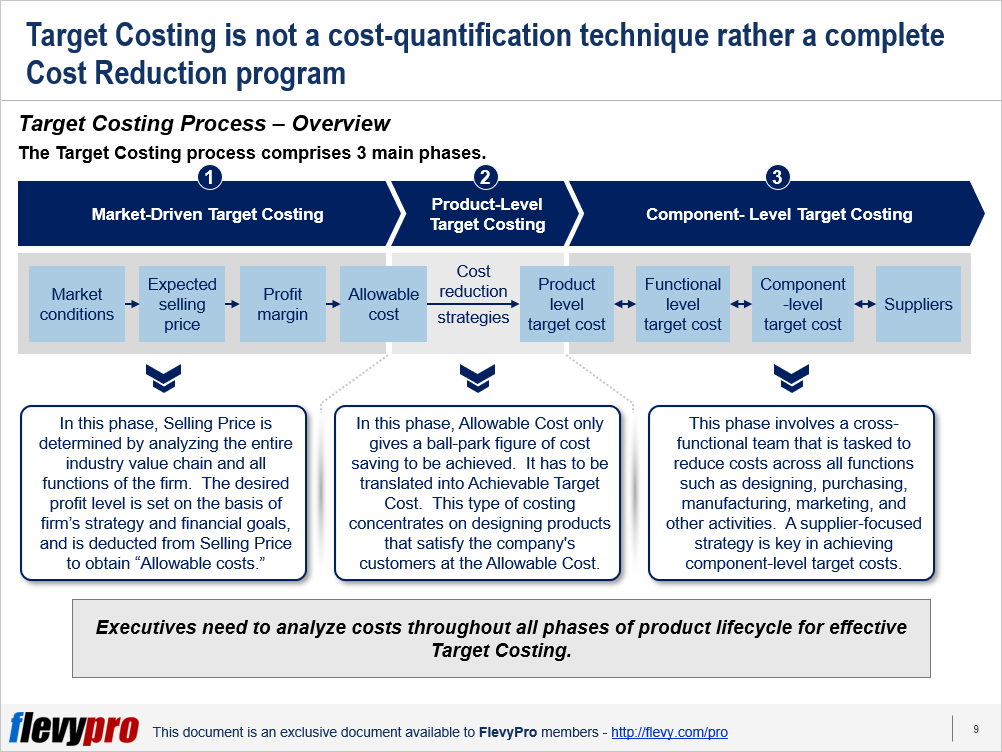

The Target Costing process comprises 3 main phases.

Let’s discuss the 3 phases briefly.

In this phase, Selling Price is determined by analyzing the entire industry value chain and all functions of the firm. The focus of this costing phase is on analyzing market conditions and determining the company’s Profit Margin in order to identify the “Allowable Cost” of a product.

In this phase, the desired profit level is set on the basis of firm’s strategy and financial goals, and is deducted from Selling Price to obtain Allowable costs. Intensity of competition, nature of customers, similar product introduction by competitors, and level of customer sophistication are the key factors influencing Market-driven Target Costing.

In this phase, Allowable Cost only gives a ball-park figure of cost saving to be achieved. It has to be translated into Achievable Target Cost. This type of costing concentrates on designing products that satisfy the company’s customers at the Allowable Cost. The cardinal rule of Product-level Target Costing is to never exceed the Target Cost.

The objective of this Target Costing phase is to create intense but realistic pressure on the product designers to reduce costs. Product Strategy (number of products in the line, frequency of redesign, degree of innovation) and product characteristics (complexity, magnitude of up-front investments, and duration of product development) are the key factors affecting Product-level Target Costing.

The Component-level Target Costing settles the price at which a firm is willing to purchase the externally-acquired components being used in its product. This phase involves a cross-functional team that is tasked to reduce costs across all functions such as designing, purchasing, manufacturing, marketing, and other activities.

The components cost history serves as the starting point for estimating the new component-level target costs alongside optimal selection of suppliers. A supplier-focused strategy is the key factor that influences Component-level Target Costing.

Interested in learning more about how the Target Costing process works and its key steps? You can download an editable PowerPoint on Target Costing here on the Flevy documents marketplace.

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

There is a general belief among organizations that a large percentage of a product’s costs are locked in by design. It is assumed that little can be done once the  design is set. This assumption has influenced cost management programs across diverse products’ life cycles. As a result, the focus during the design phase is Cost Reduction and Cost Containment during the manufacturing phase.

design is set. This assumption has influenced cost management programs across diverse products’ life cycles. As a result, the focus during the design phase is Cost Reduction and Cost Containment during the manufacturing phase.

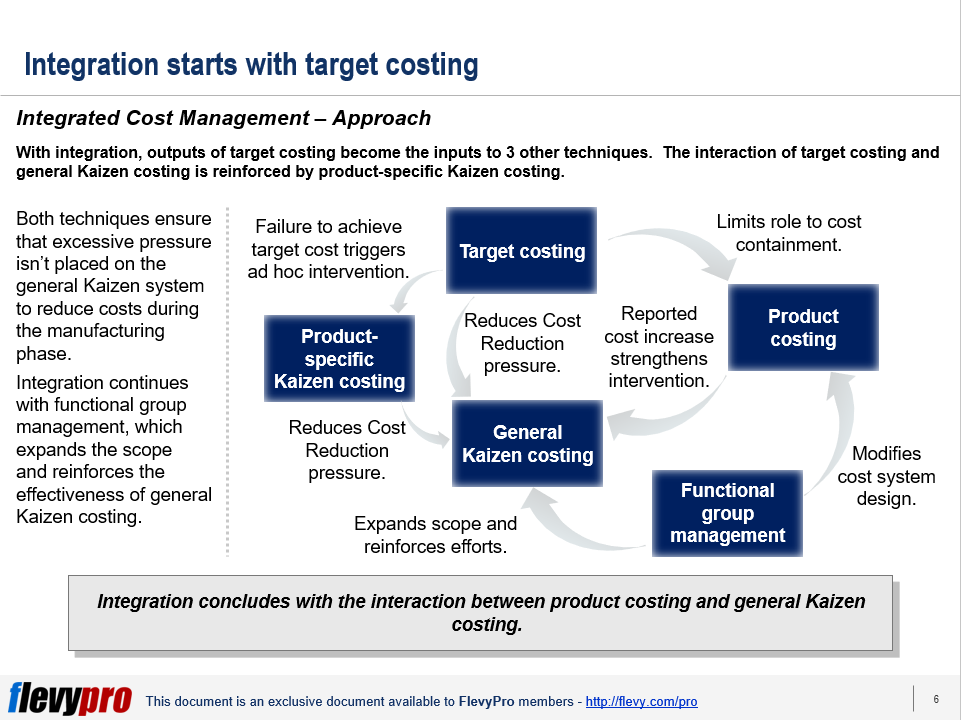

Yet, organizations that operated in a highly competitive market and demanded aggressive cost management showed that costs can be aggressively managed throughout the product life cycle. Various cost management strategies or techniques may be used to increase the program’s overall effectiveness. One of them is the Integrated Cost Management.

Integrated Cost Management is every organization’s prescription for lower cost and higher profits. It is the 21st business approach to achieving Cost Management efficiency.

Integration is necessary for Strategy Development as it can promote the achievement of the company’s profit objectives. In fact, there are major benefits to Integrated Cost Management. One of which is lowering of overall costs throughout the product life cycle.

Integrated Cost Management can facilitate a steady decrease in costs all the way to discontinuance. In fact, it can result in an annual cost reduction of about 17% during manufacturing, savings that exceed 30$%, and a designed-in cost of below 70%.

Achieving this requires an understanding of the Integrated Cost Management Approach.

The Integrated Cost Management Approach focuses on the integration of cost management techniques which can lead to higher levels of cost reduction and superior overall performance.

The Integrated Cost Management Approach takes into consideration 5 Cost Management Strategies.

The 5 Cost Management Strategies enable organizations to better manage costs throughout the product life cycle, with just one (1) technique taking place during the product design and the rest during manufacturing.

The application of the 5 Cost Management strategies has its key takeaways. These can be used as a guidepost in its application and a model of general concepts that organizations may consider.

One key takeaway is significant savings can still be achieved with short life cycle products and aggressive cost management focused on product design. Taking to note this key takeaway, we have to consider that as the length of the manufacturing phase of the product’s life cycle increases, the opportunity for cost reduction increases. Further, there is a need to explore the value of integrating multiple cost management during manufacturing.

Interested in gaining more understanding of Integrated Cost Management? You can learn more and download an editable PowerPoint about Integrated Cost Management here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.