Editor’s Note: If you are interested in becoming an expert on Strategy Development, take a look at Flevy’s Strategy Development Frameworks offering here. This is a curated collection of best practice frameworks based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. By learning and applying these concepts, you can stay ahead of the curve. Full details here.

* * * *

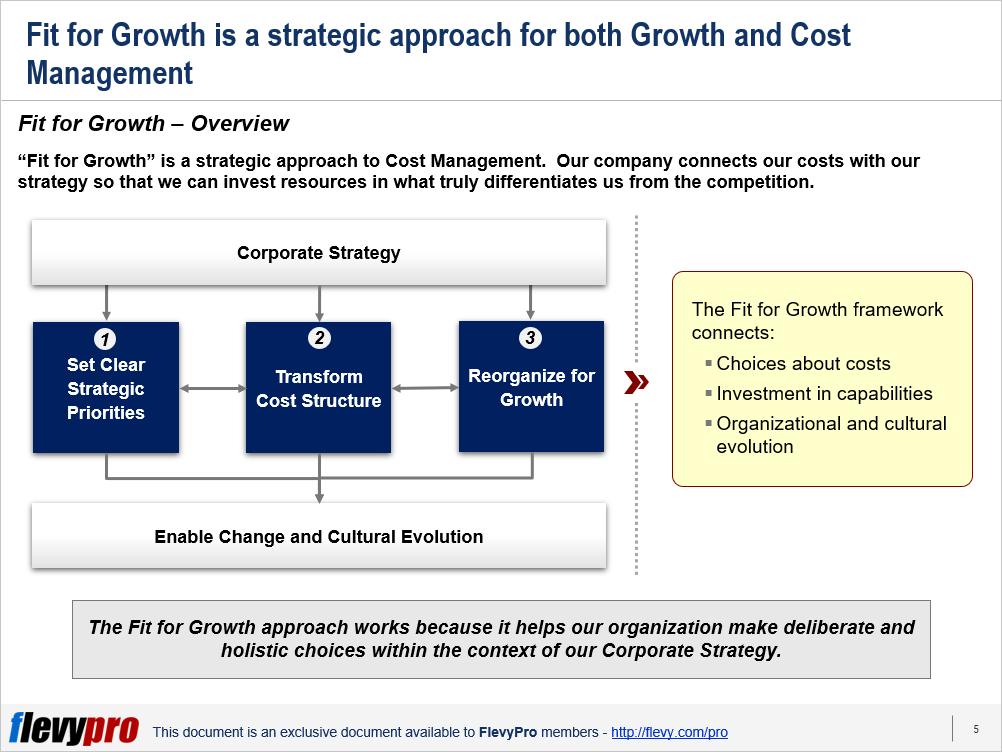

A question faced by many business leaders in today’s dynamic, uncertain, and changing business environment is: Is our organization “Fit for Growth?” In most cases, unfortunately, the answer to this question is “no.” Reasons include the manner in which costs are managed and resources deployed.

The fundamental question needed to be asked is: how to assess whether the organization is Fit for Growth? Such an assessment is effortlessly possible through answering the following 3 questions:

- Does the company have well-defined Strategic Priorities that concentrate on strategic growth and which direct its investments?

- Do the company costs align with the Strategic Priorities? i.e., efficient and effective employment of resources toward the Priorities.

- Does the Organizational Structure enable achievement of those Strategic Priorities?

Imagining the converse side of these queries makes the picture clearer. That is, what are the consequences of: Not having clear Priorities, Inappropriate deployment of Costs, Not having a well-designed organization.

Positioning the company to be Fit for Growth requires basing it on the following 3 pillars of Growth:

Setting the company on the 3 pillars enables it to direct investments towards the Capabilities that are most crucial and reduce—or eradicate—other costs.

Let us delve a little deeper into the details of these 3 pillars.

Strategic Priorities

Numerous warning indicators are apparent if the Strategic Growth Priorities of a company are not crystalized.

Warning signs such as being unable to keep track of the numerous initiatives that the company has going at the same time.

Senior executives of the company attending lots of unrelated meetings in a day. Executives being divergent on the most important capabilities of the company and how they relate to the strategic objectives.

Areas that can distinguish the company from its competitors not being properly invested in.

Research has established an important correlation between Capabilities and Strategy. Capabilities require lots of attention and investment because of their cross-functional effect and limited number.

It is therefore, needed to have clear Priority regarding which Capabilities to invest in.

Cost Structure

Inappropriate Costs Structure is also an indicator of incorrect priorities, particularly the amount spent on non-essentials.

Organizations aiming to be Fit for Growth make themselves lean and expend money purposefully. They can maintain their commanding position in such Cost Transformations by pursuing the 12 principles.

Costs are managed for efficiency as well as effectiveness using tools and practices that are usually grouped into 3 categories.

Growth

Organizations, over time, become slow in reacting to opportunities and do not move quickly enough, or are not in-line enough to work in unison. These are common manifestations, even in organizations that are run and managed well.

Interested in learning more about Fit for Growth? You can download an editable PowerPoint on Fit for Growth here on the Flevy documents marketplace.

Want to Achieve Excellence in Strategy Development?

Gain the knowledge and develop the expertise to become an expert in Strategy Development. Our frameworks are based on the thought leadership of leading consulting firms, academics, and recognized subject matter experts. Click here for full details.

“Strategy without Tactics is the slowest route to victory. Tactics without Strategy is the noise before defeat.” – Sun Tzu

For effective Strategy Development and Strategic Planning, we must master both Strategy and Tactics. Our frameworks cover all phases of Strategy, from Strategy Design and Formulation to Strategy Deployment and Execution; as well as all levels of Strategy, from Corporate Strategy to Business Strategy to “Tactical” Strategy. Many of these methodologies are authored by global strategy consulting firms and have been successfully implemented at their Fortune 100 client organizations.

These frameworks include Porter’s Five Forces, BCG Growth-Share Matrix, Greiner’s Growth Model, Capabilities-driven Strategy (CDS), Business Model Innovation (BMI), Value Chain Analysis (VCA), Endgame Niche Strategies, Value Patterns, Integrated Strategy Model for Value Creation, Scenario Planning, to name a few.

Learn about our Strategy Development Best Practice Frameworks here.

Do You Find Value in This Framework?

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of