A traditional Value Chain involves a linear sequence of activities—from conversion of raw materials into components which are assembled into products. The products are then distributed, marketed, sold, and serviced. Management plans and execute strategies and operations based on this sequence.

A traditional Value Chain involves a linear sequence of activities—from conversion of raw materials into components which are assembled into products. The products are then distributed, marketed, sold, and serviced. Management plans and execute strategies and operations based on this sequence.

This set of activities worked well for organizations in the past. However, this linear progression does not encourage Innovation and provides little protection from the risk of being outperformed by rivals in today’s disruptive markets. Such a competitive environment calls for implementing more robust ways of managing Customer Demand and Value Creation.

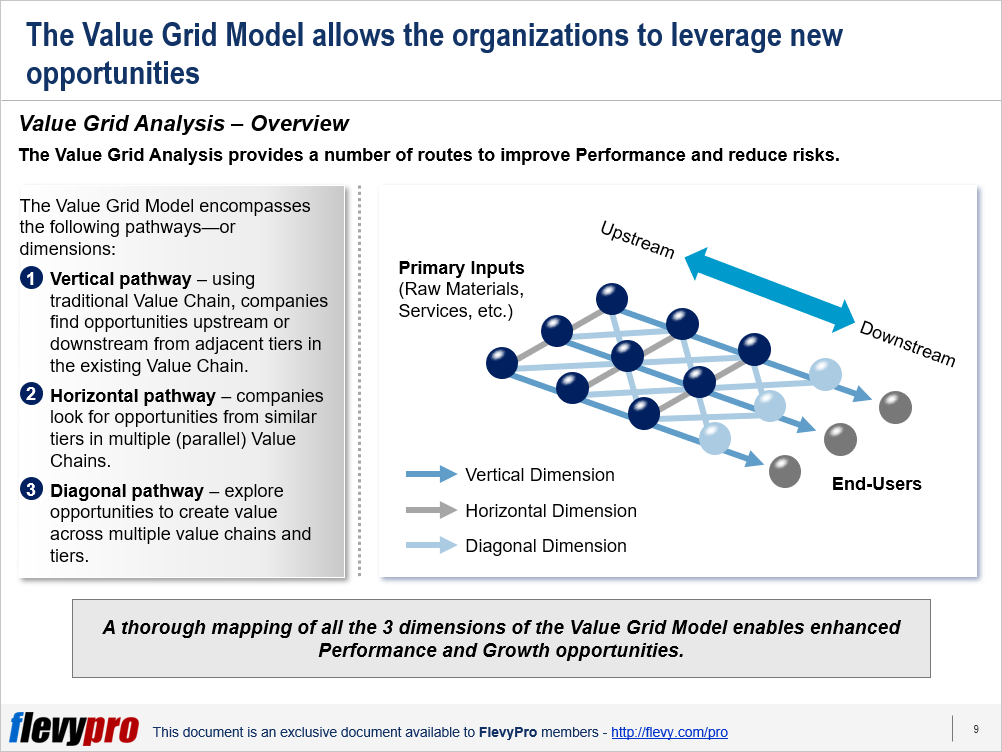

An effective approach to deal with this challenge is the Value Grid Analysis Model. The Value Grid approach provides a perspective beyond traditional linear progression of activities, where organizations need to balance equilibrium between suppliers and manufacturers aside from concentrating only on reducing lead times. It outlines new opportunities and risks for organizations.

The Value Grid Analysis provides a number of routes to improve Performance and reduce risks. It encompasses the following 3 pathways—or dimensions:

- Vertical pathway – using traditional Value Chain, companies find opportunities upstream or downstream from adjacent tiers in the existing Value Chain.

- Horizontal pathway – companies look for opportunities from similar tiers in multiple (parallel) Value Chains.

- Diagonal pathway – explore opportunities to create value across multiple value chains and tiers.

The Value Grid Framework necessitates diverting leadership attention towards 3 key opportunity areas to create Competitive Advantage:

- Customer Demand

- Information Access

- Multi-tier Penetration

Let’s dive deeper into the 3 opportunity areas.

Customer Demand

The first opportunity area to drive competitive advantage pertains to controlling internal and external customers’ demand. It warrants a company to manage customer demand upstream (suppliers and companies that supply to suppliers) as well as downstream (customers). By managing customer demand downstream, organizations control the decision makers responsible for the purchase decision. When companies are unable to control the decision makers, they look for levers across the Value Chain to influence decisions. These levers include direct advertisements to the end users, focusing on distributors, or incentivizing retailers to recommend a product. Organizations also try to influence upstream, e.g., their R&D units, to create products which can be used in conjunction with the existing product range to boost their efficacy and benefits for the end-users, ultimately influencing consumers’ decisions downstream.

Information Access

The 2nd opportunity area involves linking information sharing to influence decision making. A few manufacturers prefer to partner with those suppliers who openly disclose the information (capabilities, flexibility, and pricing structures) of their 2nd-tier suppliers with them. This assists them in planning and helping the suppliers manage materials and prices better.

For instance, with increased tariff on imported steel and price of steel continuously going up, car manufacturers like Honda purchase steel in bulk and sell it to their suppliers at a reduced rate. This helps them keep the prices of their cars down and compete better.

Multi-tier Penetration

Nonlinear thinking (Value Grid Model) enables the organizations to determine innovative solutions beyond the scope of traditional Value Chains. To manage excess demand organizations take on multiple Value Chain tiers to control demand and buyers’ power.

Leading manufacturers evaluate multiple value chain points for their participation in order to scale. They sell not only to Original Equipment Manufacturers but also in the aftermarket. Supplying to more than one Value Chain tier allows organizations to withstand pressure from OEMs to reduce costs, demand shifts, and offers attractive margins.

Interested in learning more about the 3 opportunity areas of the Value Grid Analysis Framework? You can download an editable PowerPoint on Value Grid Analysis here on the Flevy documents marketplace.

Do You Find Value in This Framework?

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“As a small business owner, the resource material available from FlevyPro has proven to be invaluable. The ability to search for material on demand based our project events and client requirements was great for me and proved very beneficial to my clients. Importantly, being able to easily edit and tailor the material for specific purposes helped us to make presentations, knowledge sharing, and toolkit development, which formed part of the overall program collateral. While FlevyPro contains resource material that any consultancy, project or delivery firm must have, it is an essential part of a small firm or independent consultant’s toolbox.”

– Michael Duff, Managing Director at Change Strategy (UK)

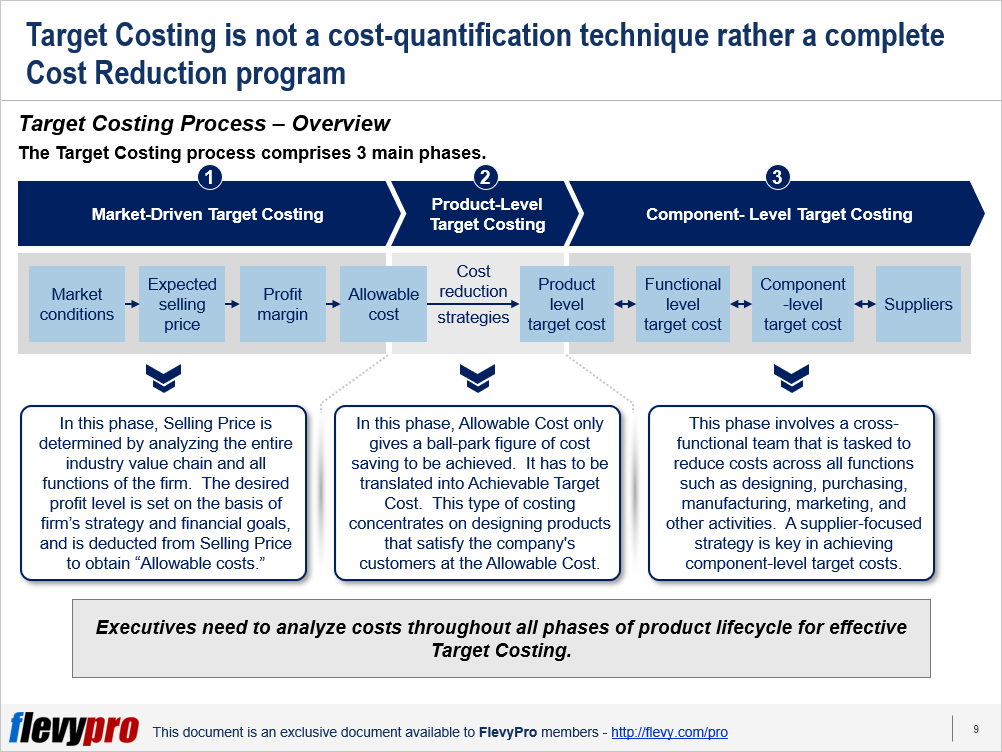

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of

Cost-based Pricing is fast becoming a relic of the past and being substituted by the concept of