Become a PowerPoint Guru by Dave Tracy

Become a PowerPoint Guru by Dave Tracy

Learn the methodologies, frameworks, and tricks used by Management Consultants to create executive presentations in the business world.

Become a PowerPoint Guru by Dave Tracy

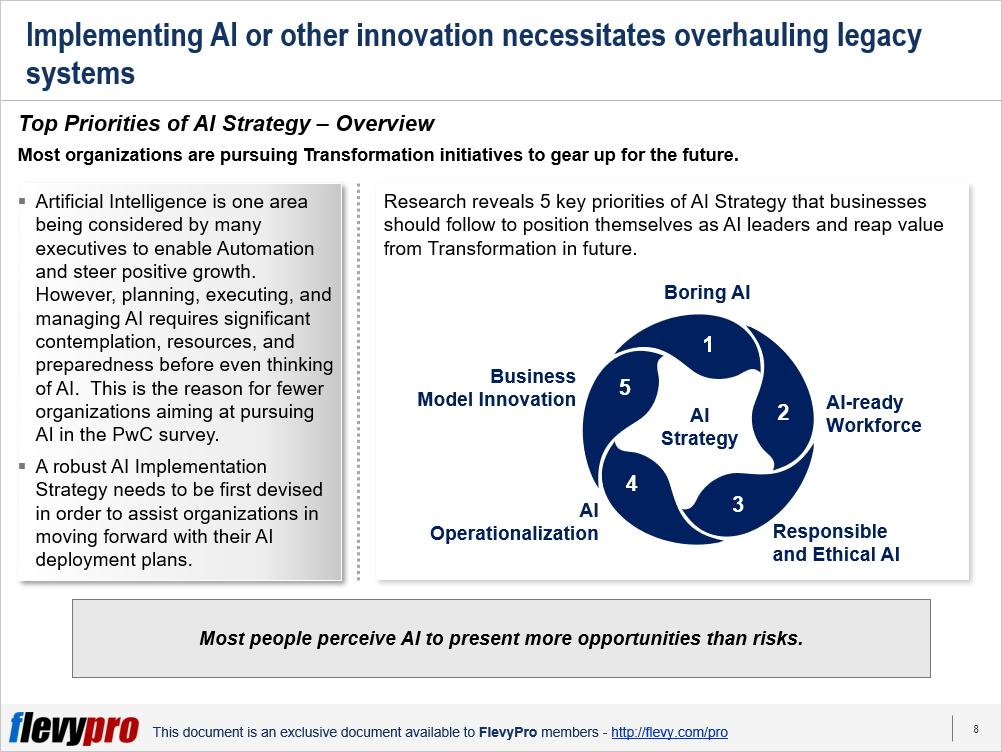

Artificial Intelligence (AI) is one area considered by many executives to enable Automation and steer positive growth. A couple of years ago, most executives thought that deployment of Artificial Intelligence isn’t a big deal. However, revamping traditional systems, implementing AI, and scaling it, in reality, is not as simple as it seems.

Artificial Intelligence (AI) is one area considered by many executives to enable Automation and steer positive growth. A couple of years ago, most executives thought that deployment of Artificial Intelligence isn’t a big deal. However, revamping traditional systems, implementing AI, and scaling it, in reality, is not as simple as it seems.

A survey by PwC Research in 2020, which gathered responses of 1062 business leaders, validates that scaling and industrializing AI is not straightforward at all. Only 4% of the respondents asserted that they plan on implementing organization-wide AI in 2020. A year earlier, the same survey revealed 20% of the executives planning to do that. The survey shows a significant decrease in the number of senior leaders thinking of executing AI.

The reason for this dwindling interest in AI deployment is mainly because of the tough prerequisites necessary—contemplation, resources, preparedness, overhauling legacy systems, and integration of technology applications—for enterprise-wide AI implementation.

A robust AI Implementation Strategy needs to be first devised in order to assist the organizations in moving forward with their AI deployment plans. Research reveals 5 key priorities of AI Strategy that businesses should follow to position themselves as AI leaders and reap value from Transformation in future. These priorities not only highlight the key requirements for AI deployment but also pinpoint ways to maximize pay offs associated with the initiative:

Let’s delve deeper into a few of these key priorities.

One of the key reasons to employ AI, as cited by PwC research, is to automate routine administrative functions—e.g., using AI to pull information from tax forms, bills of lading, or invoices that can otherwise take up long hours of human effort. 44% of respondents revealed that AI will help them operate more efficiently.

To ensure AI adds value to the business, leaders should develop a strategy to identify the areas where AI can have a much deeper impact; build capabilities to do that; develop AI solutions, govern them, and embed them with existing systems.

Building or enhancing the capabilities of the workforce to become AI ready is critical today not only for technology enterprises but also for other businesses. Organizations should identify the skills required for AI and train their people to deploy AI solutions.

However, thinking of achieving this through traditional means of offering training sessions isn’t a viable strategy to tap the opportunities offered by AI. In addition to training people, organizations should cross-skill their people in multiple trades and provide them the opportunities to apply and hone in the skills learnt. In fact, organizations should reward people who apply what they learn into real-time problem-solving and productivity enhancement.

AI can be perilous if adequate understanding of its responsible use and necessary procedures to protect against its risks and negative usage are not taken. There are growing apprehensions around AI related risks e.g., biased algorithms, facial recognition tools, and deep fakes. As per PwC survey, a large majority of respondents, using AI routinely, declared readiness in their organizations in terms of taking sufficient measures to protect against AI risks.

However, in reality most organizations are quite far from implementing controls around data and decisions generated using AI. Just about 33% businesses mentioned having the ability to fully tackle risks associated with data powering AI, AI models, outputs, and reporting. It is imperative to have rigorous Risk Management processes in place to effectively use AI in the workplace and address the risks associated with it. AI risks can be mitigated by integrating processes, tools, and controls needed to address AI bias, explainability, security, accountability, and ethics.

Interested in learning more about the other key strategic priorities essential for AI deployment readiness? You can download an editable PowerPoint on Artificial Intelligence Strategy: Top Priorities here on the Flevy documents marketplace.

You can download in-depth presentations on this and hundreds of similar business frameworks from the FlevyPro Library. FlevyPro is trusted and utilized by 1000s of management consultants and corporate executives. Here’s what some have to say:

“My FlevyPro subscription provides me with the most popular frameworks and decks in demand in today’s market. They not only augment my existing consulting and coaching offerings and delivery, but also keep me abreast of the latest trends, inspire new products and service offerings for my practice, and educate me in a fraction of the time and money of other solutions. I strongly recommend FlevyPro to any consultant serious about success.”

– Bill Branson, Founder at Strategic Business Architects

“As a niche strategic consulting firm, Flevy and FlevyPro frameworks and documents are an on-going reference to help us structure our findings and recommendations to our clients as well as improve their clarity, strength, and visual power. For us, it is an invaluable resource to increase our impact and value.”

– David Coloma, Consulting Area Manager at Cynertia Consulting

“FlevyPro has been a brilliant resource for me, as an independent growth consultant, to access a vast knowledge bank of presentations to support my work with clients. In terms of RoI, the value I received from the very first presentation I downloaded paid for my subscription many times over! The quality of the decks available allows me to punch way above my weight – it’s like having the resources of a Big 4 consultancy at your fingertips at a microscopic fraction of the overhead.”

– Roderick Cameron, Founding Partner at SGFE Ltd

Reducing the fragility of global Supply Chains in the event of disruption through natural or other disasters is a major concern for most senior executives. This rings true more so now than ever, as the world grapples with COVID-19, the worst human health crisis in 100 years.

Reducing the fragility of global Supply Chains in the event of disruption through natural or other disasters is a major concern for most senior executives. This rings true more so now than ever, as the world grapples with COVID-19, the worst human health crisis in 100 years.

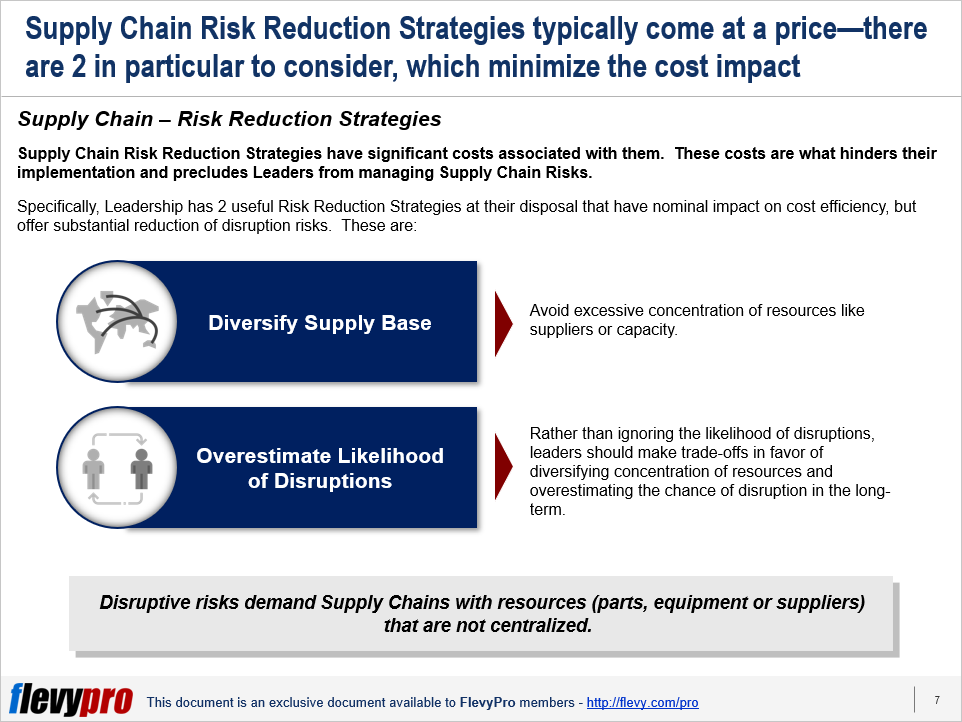

The strategies to enhance the effectiveness and readiness level of Supply Chains and to reduce risks associated with disruption come with a price. These costs are critical to build Supply Chain Resilience across all industries.

However, these expenses are, generally, considered a hindrance in the implementation of risk reduction strategies by many leaders. This is one of the major factor that precludes them from anticipating and managing Supply Chain Risks.

Able leaders anticipate these risks and invest in building organizational resilience. They leverage a couple of potent Supply Chain Risk Reduction Strategies that have nominal impact on cost efficiency but offer substantial reduction of disruption risks:

It is vital for organizations to diversify their supplier base to avoid disruption of their Supply Chains in the event of a natural disaster. Manufacturers have been found to have been using pooling—combining resources, inventory and capacity by maintaining fewer distribution centers—and producing common parts to help reduce costs. However, too much pooling and commonality can make the Supply Chain vulnerable to disruption.

For instance, relying too much on a single supplier and common parts—in an effort to be as lean and efficient as possible—became a Supply Chain Analysis nightmare and cost Toyota billions of dollars in terms of lost sales and product recalls in 2010. Back then, the auto manufacturer was counting on a single supplier for a common part for many of its car models, which was effective in curtailing costs, but turned out to be a disaster.

Organizational leadership should evaluate the trade-offs between having a leaner and efficient Supply Chain—with common parts and single suppliers—and preparing for and reducing the risks of disruptions. Minimizing the number of distribution centers offers diminishing marginal returns for Supply Chain Performance and increases the Supply Chain Fragility. Creating little bit of commonality presents significant advantages, but when more parts are made common the benefits shrink and it rather becomes detrimental.

The key for senior leaders is to find an optimal balance between resource pooling, creating common parts, and deciding on whether to decentralize or centralize their Supply Chains. Decentralization (e.g., by having multiple warehouses or plants) increases costs as it requires more inventory, but it does curtail the effect of disruption significantly. Centralization or pooling of resources, on the other hand, reduces total costs, but the cost again goes up by centralizing beyond a reasonable degree. Recurrent Supply Chain Risks necessitate focusing more on centralization and pooling of resources and commonality of parts, while rare disruptive risks necessitate decentralization. Achieving a state of equilibrium between pooling of resources, parts commonality or fewer plants helps keep Supply Chain Risks low. Ignoring the possibility of disruption can be very expensive in the long term. Samsung Electronics Co. Ltd. always maintain at least two suppliers, no matter if the second supplier supplies only a fraction of the volume.

The risk of disruption of supply chains due to any unforeseen event is typically considered a rare possibility and goes unaccounted for during planning by most executives. A fire break out at a distribution center, defective auto part, or a supplier’s facility closure for a prolonged period of time can happen anywhere, but we tend to underestimate the likelihood of such events. The reason for this is attributed to the requirement of assigning a significant chunk of investments upfront from the already limited resources and budgets, to prepare for and mitigate likely disruptive risks.

Most of our typical risk assessment measures involve approximating the probability and the likely damage caused by an event. Estimating the likelihood of disruptive risk to a reliable degree isn’t easy even for large multinationals—even an auto manufacturer like Toyota could not anticipate the occurrence of the part failure issue until the damage had been done. These risk estimations do not have to be strictly precise. Rough estimates of disruption risk are fine—any small mis-estimates that occur have negligible consequences.

Senior leadership needs to cautiously contemplate the areas that are likely to get affected the most due to potential disruption. Building resilience does not cost much for large organizations. In the long term, doing nothing costs much more than investing in preparing for a probable disruption. When disruption occurs, the loss incurred greatly exceeds the amount of saving executives save by not investing in risk mitigation strategies.

Interested in learning more about the subject in detail? You can download an editable PowerPoint on Supply Risk Reduction Strategies here on the Flevy documents marketplace.

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

Supply Chains often get disrupted by calamities that are beyond human control. Natural disasters, such as tsunamis and floods, in the last decade have drastically affected major businesses—from automobiles to technology, to travel, to shipments—and exposed critical weaknesses in Supply Chain mechanisms around the globe. And, now, we are living through a global disruption of an unparalleled nature, COVID-19.

Organizations that rely on single-source suppliers, common parts, and centralized inventories are more susceptible to the risk of disruption.

Management in most cases is aware of its responsibility to prevent their Supply Chains from getting disrupted by ensuring measures such as keeping enhanced stocks, improving capacity at discrete facilities, and choosing multiple sources. But these measures have a negative effect on Supply Chain cost efficiencies.

However, discerning the effects of costly Supply Chain disruptions is one thing and taking actions to avoid such situations or mitigating their undesirable effects is another. Managing Supply Chain risks necessitates careful evaluation of the impact that these measures have on Supply Chain cost efficiencies and bottom line. During the COVID-19 pandemic, it has become clearer than ever that Supply Chain Management must also involve this form of Risk Management.

Supply Chain Efficiency entails improving the financial performance of an organization and focusing on improving the way we manage supply and demand. Demand fluctuations or supply delays are independent and can be typically tackled by having appropriate inventory levels in the right place, better planning and implementation, and improving Supply Chain Cost Efficiency.

Supply Chains are complex operations encompassing many products or commodities that are sourced, manufactured or stored in multiple locations. These complexities can slash efficiency, cause delays, suspension of operations, and increased risk of disruption. Containing complexities brings higher cost efficiencies and reduced risks.

Supply Chain Containment ensures that Supply Chain disruptions caused by internal factors or through natural hazards are contained within a portion of the Supply Chain. A single Supply Chain for the entire organization seems cost effective in the short term, but even a small issue can trigger a disaster.

Supply Chain Containment Strategies are useful for the organizations to design and deploy solutions fairly quickly in the event of disruption through natural disasters. The objective is to limit the impact of disruption through disasters to a minimum—to just a portion and not the entire Supply Chain.

For instance, in order to reduce the impact of parts shortage, a mechanical parts manufacturer should arrange multiple supply sources for common items or limit the number of common items across different models. To reduce Supply Chain instability and to improve financial performance, organizations can use the following containment strategies:

The basis for Supply Chain segmentation are volume, product diversity and demand uncertainty. High margin but low-volume products with high-demand uncertainty warrant keeping Supply Chains flexible, with capacity that is centralized to aggregate demand. Manufacturing everything in high-cost locations is detrimental to profit margins. Sourcing responsive suppliers from Europe is a model feasible for trendy high-end items only. For fast-moving, low margin, basic products it is sensible to source from multiple low-cost suppliers. Centralization is favorable in case of fewer segments, significant product variety, low sales volumes of individual products, and high demand uncertainty to achieve reasonable levels of performance. Decentralization is suitable in case of higher sales volumes, less demand uncertainty, and more segments, to help become more responsive to local markets and reduce the risk of disruption. For instance, utility companies utilize low-cost coal-fired power plants to handle predictable demand, whereas employ higher-cost gas- and oil-fired power plants to handle uncertain peak demand.

Supply Chain Regionalization helps curtail the impact of losing supply from a plant within the region. For instance, Japanese automakers were badly hit by shortage of parts globally in the event of 2011 tsunami, since most of these parts could be sourced only from storage and distribution facilities in the tsunami-affected regions. Had they operated with decentralized regional Supply Chains with logistics centers dispersed in various locations they would have significantly contained the impact of disruption.

Supply Chain Regionalization lowers distribution costs while also reducing risks in global Supply Chains. During periods of low fuel and transportation costs, global Supply Chains minimize costs by locating production where the costs are the lowest. As transportation costs rise, global Supply Chains may be replaced by regional Supply Chains. Regionalized Supply Chains with same inventory stored in multiple locations appear wasteful, but are more robust in case one of the logistics centers suffers from a disaster.

Interested in learning more about the Supply Chain Segmentation and Regionalization? You can download an editable PowerPoint on Supply Chain Containment Strategies here on the Flevy documents marketplace.

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

Enterprises invest in Analytics to improve Decision Making and outcomes across the business. This is from Product Strategy and Innovation to  Supply Chain Management, Customer Experience, and Risk Management. Yet, many executives are not yet seeing the results of their Analytics initiatives and investments.

Supply Chain Management, Customer Experience, and Risk Management. Yet, many executives are not yet seeing the results of their Analytics initiatives and investments.

Every organization putting on investment in Analytics has experienced several stumbling blocks. This differentiates the leaders from the laggards. Analytics-driven Organizations have clearly established processes, practices, and organizational conditions to achieve Operational Excellence. Their commitment to Analytics is creating a major payoff from their investments and a competitive edge.

The Harvard Business Review Analytic Services conducted a survey of 744 business executives around the world and across a variety of industries. Their focus was on the performance gap between companies that have struggled to get a return on their Analytics investment and those that have effectively leveraged their investment.

The survey showed that Analytics-driven Organizations get sufficient return on investment in Analytics. In fact, they have been highly successful in gaining a return on Analytics investment. This is gainfully achieved as organizations use Analytics consistently in strategic decision making. Executives of Analytics-driven Organizations rely on Analytics insights when it contradicted their gut feel.

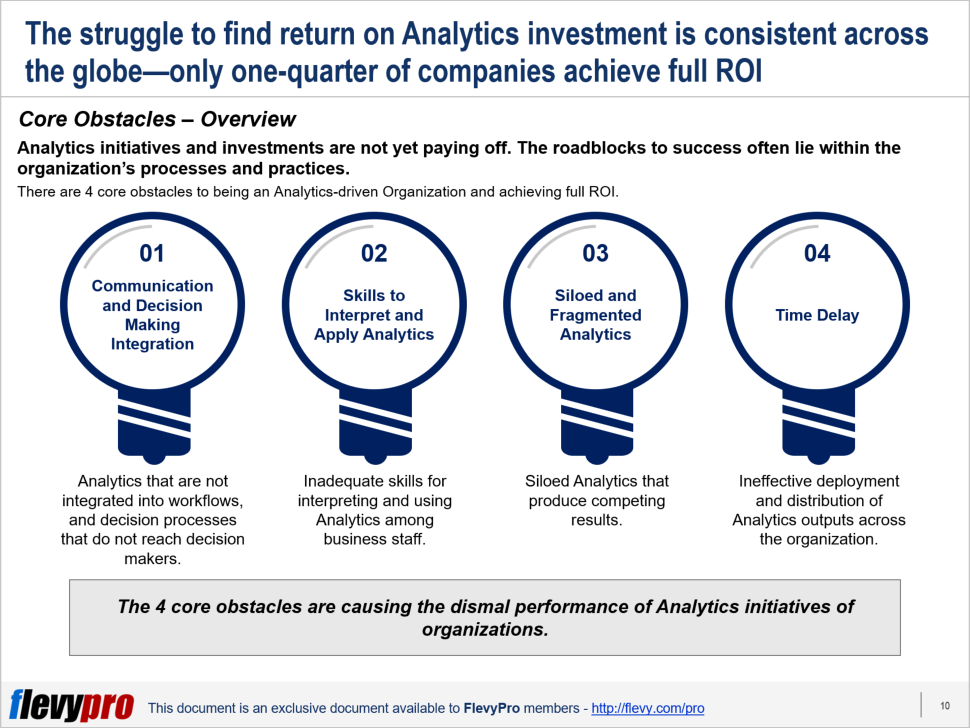

Essentially, Analytics-driven Organizations have reduced costs and risks, increased Productivity, Revenue, and Innovation, and have successfully executed their Strategy. Yet, in evolving the organization’s Analytics approach, there can be 4 core obstacles that can affect their drive to getting a greater return on investment in Analytics.

There are 4 core obstacles to being an Analytics-driven Organization.

Let’s briefly take a look at the first 2 obstacles:

The other two core obstacles are siloed and fragmented Analytics and time delay. These are two equally important core obstacles that can hinder the use of Analytics to maximize return on investment. Further, the 4 core obstacles are barriers to analytic success.

Leaders use Analytics consistently in decision making. In fact, based on the survey, 83% of executives use it in business planning and forecasting. On the other hand, laggards only use it 67% of the time. Even in various aspects of the organization such as Marketing, Operations, Strategy Development, Sales, Supply Chain, Pricing and Revenue Management, and Information Technology, laggards use Analytics only half the time compared to Analytics Leaders.

Analytics Leaders always ensure that they establish the processes and organizational conditions to allow them to successfully deploy Analytics. In fact, to increase return on Analytics, organizations must undertake the use of four interrelated initiatives that will drive greater return on investment Analytics. These are four initiatives essential to building an Analytics-driven Organization.

One is building an organizational culture around Analytics. To achieve this the organization must have clear, strategic, and operational objectives that are set for Analytics. Second is deploying Analytics throughout all core functions of the business.

Starting with an Analytics-driven Culture can greatly facilitate cross-functional deployment of Analytics.

Interested in gaining more understanding of Analytics-driven Organization? You can learn more and download an editable PowerPoint about Analytics-driven Organization here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

When things go wrong on a grand scale, often we direct our attention to the role of the Board. Debate exudes and often gets heated up and  intensifies. This often happens when the Board spends more time looking in the rearview mirror and not enough scanning the road ahead. When this happens, governance suffers.

intensifies. This often happens when the Board spends more time looking in the rearview mirror and not enough scanning the road ahead. When this happens, governance suffers.

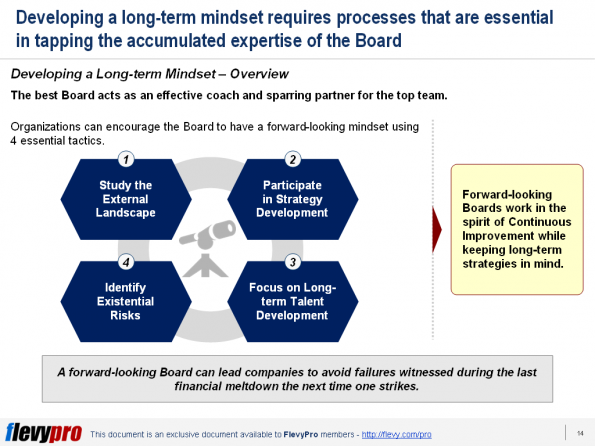

Often, the Board of Directors spend a bulk of its time on quarterly reports, audit reviews, budgets, and compliance. However, with the change in the business environment, there is a greater need to redirect the Board’s attention on matters crucial to the future prosperity and direction of the business. One of this is Strategy Development. Achieving this requires the development of a dynamic Board with a long-term mindset capable of creating forward-looking agenda and activities that get sufficient time over a 12-month period.

The Board Agenda is changing. It is becoming more dynamic and it has increasingly highlighted forward-looking activities. Long-term economic, technological, and demographic trends are radically shaping the global economy. The second Industrial Revolution now requires the Board to shift focus. The Board is now challenged to focus on matters crucial to achieving Operational Excellence and the future direction of the organization. Directors must devote more time to strategic and forward-looking aspects of the agenda. They must cease seeing the job as supporting the CEO, but instead, be strategic in making sure long-term goals are formulated and met.

Having a forward-looking Board has now become every organization’s imperative. However, this can only be achieved if there is a solid foundation that is anchored on three guiding principles. Organizations must have the right Board Member, a clear definition of the Board’s role, and greater time commitment from members. At this time when a long-term mindset has come to a fore, these have become essential.

“Strategy without tactics is the slowest route to victory. Tactics without strategy are the noise before defeat.” – Sun Tzu

Organizations can undertake 4 essential tactics to encourage the Board to have a long-term mindset.

The 4 tactics are essentially effective in creating long-term mindsets. When this is achieved, Board Excellence is never far behind.

Interested in gaining more understanding of achieving Board Excellence via a Long-term Mindset? You can learn more and download an editable PowerPoint about Board Excellence: Long-term Mindset here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

The pressure on Boards and Directors to raise their game has remained acute. A survey of more than 770 directors from public and private  companies across the industries around the world suggested that some are responding more energetically than others.

companies across the industries around the world suggested that some are responding more energetically than others.

There is a dramatic difference between how directors allocate their time among boardroom activities and the effectiveness of the Boards. One in four directors assessed their impact as moderate or lower, while others reported as having a high impact across Board functions.

Today, the call to become more forward-looking and achieving Board Excellence is further highlighted. This is further emphasized when the Board and Management are pressured to find the best answers to global business concerns and issues. In Strategy Development, this becomes invaluable. It does not only lead to clearer strategies but also the creation of alignment essential in making bolder moves.

While these are essential, there is a need to raise the quality of engagement on strategy between the Board and Management for each group to achieve smarter options. This is possible only if organizations have high impact, strategic Boards in place.

High impact, strategic Boards have a greater impact as they move beyond the basics and face increasing challenges.

Business is fast-changing and rapidly transforming. The global economy is increasingly pushing businesses, as well as the Board to face a gamut of challenges.

What are the 2 main challenges facing Boards today?

First is Time Commitment. Working at a high level takes discipline – and time. In fact, the greater time commitment is expected on high impact activities. The Board often have 6 to 8 meetings a year. As a result, they are often hard-pressed to get beyond the compliance-related topics to secure the breathing space needed for developing a strategy.

Often, it is the very high impact Directors who invest more time compared to moderate or lower average Directors.

Who are your very high impact Directors? They are those spend a total of 40 days a year working for the Board compared to 19 days of low impact Directors. An extra 8 workdays a year is invested in strategy and an extra 3 workdays a year are spent on Performance Management, M&A, Organizational Health, and Risk Management.

High impact Directors who believe that their activities have greater impact spend significantly more time on these activities compared to low impact Boards.

Second is Strategy Understanding. Why is Strategy Understanding a challenge for the Board? Limited understanding of the organization’s strategy can result in the Board’s limited engagement with the organization. Based on the survey made, only 21% of the Directors have a complete understanding of the current strategy. Often, Board members have a better understanding of the company’s financial position rather than its risks or industry dynamics.

If we look at high impact Directors, they invest more time in dealing with strategic issues. In fact, they invest 8 extra workdays a year on Strategic Planning and discussing strategy compared to low impact Directors. High impact Directors center on Strategy Focus Areas which can, in turn, spur high-quality engagement from the Board on strategy development. The quality of Board engagement on strategy is enhanced, both when the engagement is deep and during the regular course of business.

The Board just needs to focus on 3 areas of discussion for the Board to enhance Strategy Development. One of them is Industry and Competitive Dynamics.

Interested in gaining more understanding of Board Excellence via High Impact, Strategic Boards? You can learn more and download an editable PowerPoint about Board Excellence: High Impact, Strategic Boards here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

The use of the Internet and other online tools have turned consumers to be more empowered and are now shopping differently. Customers are  becoming more demanding and accustomed to getting what they want.

becoming more demanding and accustomed to getting what they want.

With greater access to reviews and online rating, customers are better equipped to switch to new products and services. Consumers now want to buy products and services when, where, and however they like. They expect companies to interact with them seamlessly, in an easy, integrated fashion with very little friction across channels.

As customer expectation continues to evolve–accelerated by the amplifying forces of interconnectivity and technology–markets are becoming increasingly fragmented with demand for greater product variety, more price points, and numerous purchasing and distribution channels.

Companies should be able to adapt to these increasingly disparate demands quickly and at scale. Staying close to the Customer Experience across an increasingly diverse customer base changing over time is no longer a matter of choice. It is a business imperative and a matter of corporate survival.

The Age of the Customer now calls for companies to be a Customer-centric Organization. Successful ones have discovered that driving customer-centricity depends, first and foremost, on building a Customer-centric Culture.

In the Age of the Customer, business as usual is not enough. Customers expect companies to interact with them seamlessly. Customers want companies to anticipate their needs and technology must have lowered barriers to entry to allow unorthodox competitors to disrupt markets.

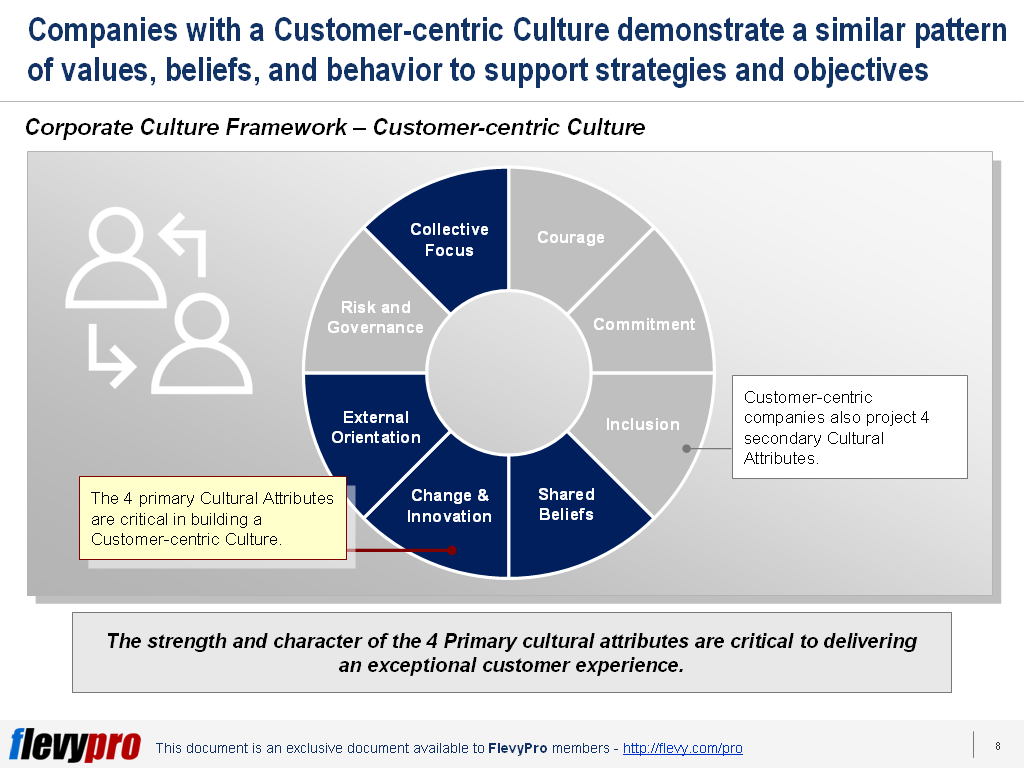

The Age of the Customer has made it imperative for companies to have a customer-centric culture. A Customer-centric Culture can empower and control employee behavior. It is a culture that prioritizes the common understanding, sense of purpose, emotional commitment, and resilience. It is a culture where leaders and employees understand the company’s brand promise. Finally, and most importantly, a customer-centric culture is a culture that is committed to delivering exceptional customer experience.

Companies with a Customer-centric Design must integrate, within its core, primary and secondary cultural attributes essential to complete its customer-centric culture framework.

In a customer-centric Corporate Culture framework, the primary cultural attributes are critical in building a customer-centric culture. It also has 4 Secondary Cultural Attributes to complete that transformation.

Inculcating these attributes has become imperative to achieve a successful transformation towards a Customer-centric Culture. Strategy Development now requires organizations to master the necessary practices to instill these attributes and the essential reinforcement to ensure that it is sustained.

Interested in gaining more understanding of Customer-centric Culture? You can learn more and download an editable PowerPoint about Customer-centric Culture here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

Companies face increasing pressure from governments, competitors, and employees to play a leading role in addressing a wide array of  environmental, social, and governance issues in a company’s supply chain. It could range from climate change to obesity to human rights.

environmental, social, and governance issues in a company’s supply chain. It could range from climate change to obesity to human rights.

For the past 30 years, companies have responded by developing corporate social responsibility or sustainability initiatives to fulfill their contract with society by addressing these issues.

However, gathering the data needed to justify sustained, strategic investment in programs can be difficult. Yet, without this information, executives and investors often see programs as separate from a company’s core business or unrelated to its shareholder value. While there are companies that have made progress tracking operational metrics or social indicators, they have difficulty linking such metrics and indicators to a real financial impact.

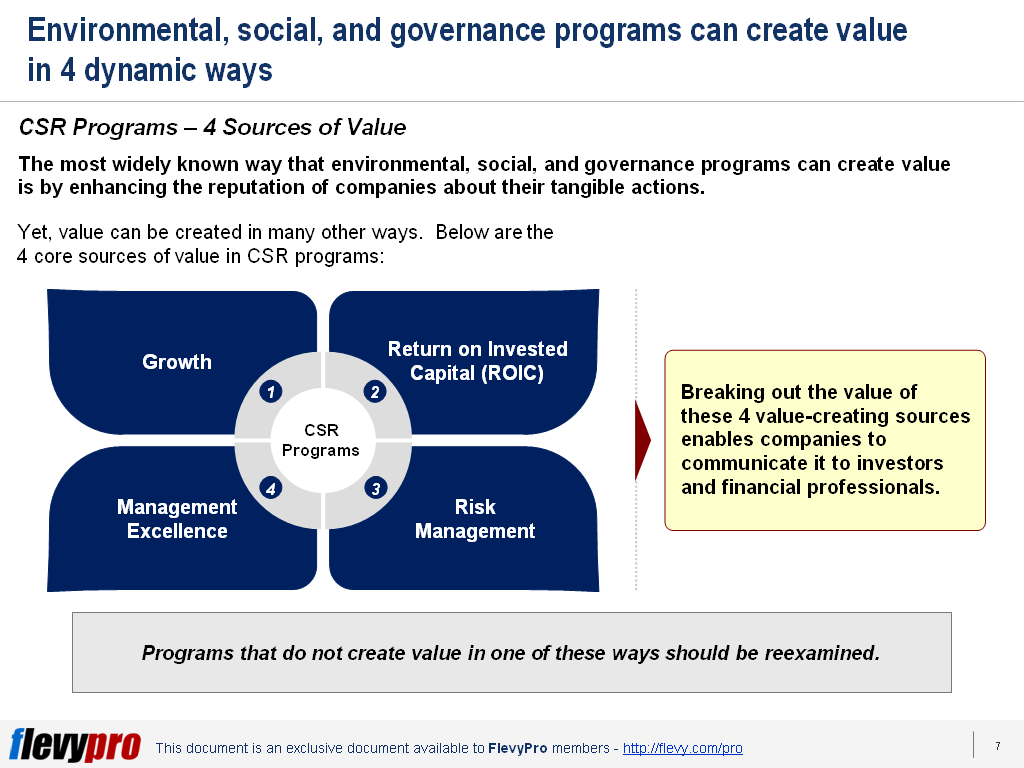

Needless to say, there are companies that are creating great value through environmental, social, and governance activities. Increased sales, decreased costs, and reduced risks are being achieved. Environmental, social, and governance programs can create value in many other ways. We just need to know where and how.

Corporate Social Responsibility (CSR) or sustainability initiatives are undertaken to fulfill contracts with society to respond to environmental issues. Environmental, social, and governance refer to a broader set of CSR Programs.

Sustaining strategic investments in CSR Programs can be a challenge but there are already leading companies that are generating real value through environmental, social, and governance activities.

CSR Programs can create shareholder value. It is just important that companies must broaden their legitimacy in societies where they operate.

IBM has been recognized globally as one of the leading companies when it comes to Information Technology. In creating new markets, IBM used Small and Medium Enterprise (SME) Toolkit to develop a track record with local stakeholders, including local governments and NGOs. Free web-based resources on business management were provided to SMEs in developing economies. A total of 30 SME Toolkit sites were developed in 16 languages.

As a result of this initiative, IBM’s reputation and relationships in new markets improved. Likewise, the relationship with companies that are potential customers was developed. The strategic approach of IBM in creating markets through its CSR has provided IBM much value in creating and developing relationships which are essential in new markets.

Interested in gaining more understanding of sources of value to CSR programs? You can learn more and download an editable PowerPoint about Corporate Social Responsibility (CSR): Sources of Value here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

Big cross-organizational change can be difficult and not all organizational transformation is the same.

Rapid advances in technology, a growing global creative workforce, and market with fewer and fewer barriers to entry are driving a hyper-creative volatile marketplace. New ideas are making established business positions obsolete at an increasing rate. Products and services that survive are exposed to commodifying price pressure.

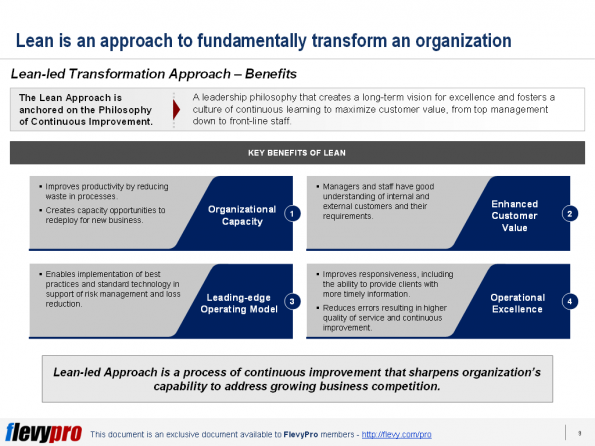

The world has started to repeatedly demand operational excellence not only in innovation but in the delivery of customer service. Continuous improvement has been deeply emphasized with the increasing demand in the marketplace. Companies must recognize the fundamental market shifts that are occurring and must learn to respond effectively. This can be done by building an organization that discovers, shapes, and brings Lean-led Business Transformation to scale as part of its core business direction and purpose.

Lean-led Business Transformation provides the business the institutional capability and framework to adapt to rapidly changing opportunities

Understanding the Lean-led Approach

An approach based on Lean Thinking provides business tangible results that are evident in financial performance, customer and employee satisfaction, and risk mitigation.

From Lean-led Approach to Lean-led Transformation

Companies are increasingly under pressure to cut costs and grow. Applying the Principles of Lean Management allow companies to fundamentally transform their operating models.

Using a Lean-led Business Approach, the company can effectively undertake a Lean-led Business Transformation. An effectively undertaken Lean-led Business Transformation can help the company build a robust, factual understanding of its current state, exposing improvement opportunities to design an end-state operating model with enabling capabilities.

In effect, the company can achieve insurmountable results that competitors will find difficult to follow.

A Lean-led Business Transformation embeds continuous improvement in the organization. It engages employees to help business leaders successfully govern and execute change.

What Companies are Facing Today

Changing market trends have pushed companies towards Lean-led Transformation. These market trends are adding pressure on companies to simultaneously cut costs and grow.

These changing market trends are here to stay and more trends will soon evolve and affect business. Failure to heed these market trends can lead to decreased margins and profitability that can be highly detrimental to business.

Undertaking this form of Business Transformation can drive businesses to undertake executable Lean Programs that will strengthen their capability to meet these challenges.

Interested in gaining more understanding of Lean-led Business Transformation? You can learn more and download an editable PowerPoint about Lean-led Business Transformation here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.