Become a PowerPoint Guru by Dave Tracy

Become a PowerPoint Guru by Dave Tracy

Learn the methodologies, frameworks, and tricks used by Management Consultants to create executive presentations in the business world.

Become a PowerPoint Guru by Dave Tracy

Organizations can change over the years. Change may happen because that is what the customers expect or it is because the organization gets to have even the most  coveted skills. Despite the changes, there are those that stay the same—the organization’s brand, its unique culture, and its shared lexicon. These are the underlying organizational and cultural design factors that define an organization’s personality. Metaphorically, these are called Organizational DNA. The Organizational DNA can indicate whether the organization is strong or weak in executing strategy.

coveted skills. Despite the changes, there are those that stay the same—the organization’s brand, its unique culture, and its shared lexicon. These are the underlying organizational and cultural design factors that define an organization’s personality. Metaphorically, these are called Organizational DNA. The Organizational DNA can indicate whether the organization is strong or weak in executing strategy.

Today, execution has come to a fore as organizations fail to effectively implement strategies. Organizations now realize that it must first resolve this dysfunction by understanding how the inherent traits of an organization influence and even determine each individual’s behavior. The idiosyncratic characteristics of an organization can be codified using the DNA. When the DNA of an organization is purely configured, unhealthy symptoms and counterproductive behaviors are demonstrated. High performing organizations have shown that there are precepts that they closely follow to ensure that their Organizational DNA is in order.

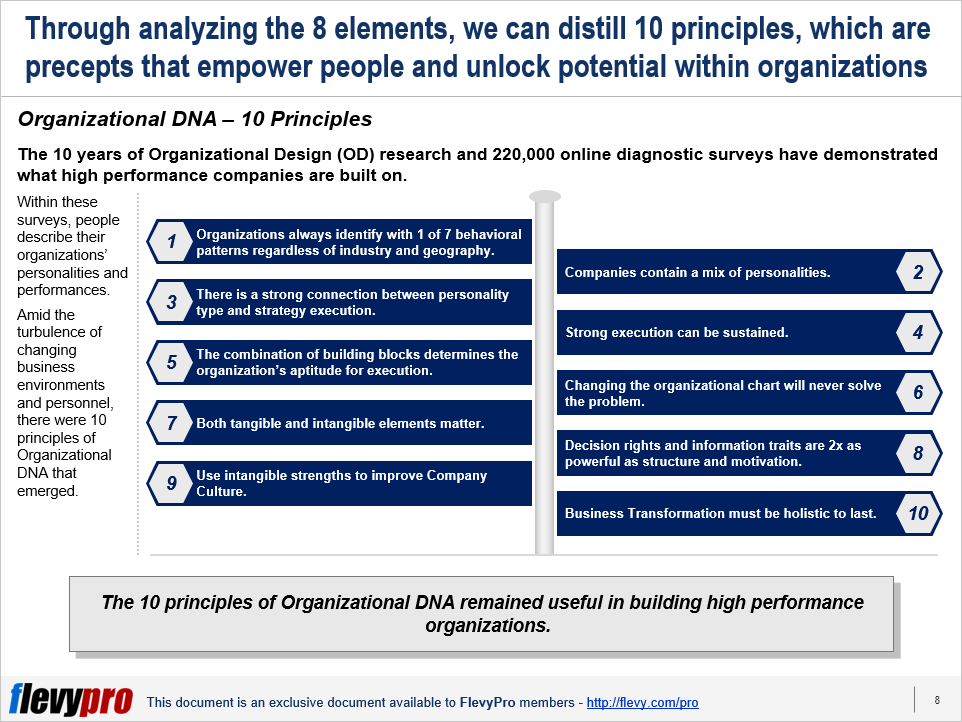

The 10 Principles of Organizational DNA are the precepts upon which high-performance companies are built on.

Let us take a look at 5 of the 10 Principles of Organizational DNA.

The other 5 core principles of Organizational DNA are essentially necessary. Even the company with the most desirable profile, the resilient organization, must continually stay at the top of the game. Hence, it is essential that organizations must adopt the most appropriate behavioral pattern and personality to be able to build high-performance organizations. Strategy Development must be able to integrate into the organization’s Business Transformation the 10 core principles of Organizational DNA.

Interested in gaining more understanding of these principles of Organizational DNA?? You can learn more and download an editable PowerPoint about Organizational DNA: 10 Core Principles here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.

There is a general belief among organizations that a large percentage of a product’s costs are locked in by design. It is assumed that little can be done once the  design is set. This assumption has influenced cost management programs across diverse products’ life cycles. As a result, the focus during the design phase is Cost Reduction and Cost Containment during the manufacturing phase.

design is set. This assumption has influenced cost management programs across diverse products’ life cycles. As a result, the focus during the design phase is Cost Reduction and Cost Containment during the manufacturing phase.

Yet, organizations that operated in a highly competitive market and demanded aggressive cost management showed that costs can be aggressively managed throughout the product life cycle. Various cost management strategies or techniques may be used to increase the program’s overall effectiveness. One of them is the Integrated Cost Management.

Integrated Cost Management is every organization’s prescription for lower cost and higher profits. It is the 21st business approach to achieving Cost Management efficiency.

Integration is necessary for Strategy Development as it can promote the achievement of the company’s profit objectives. In fact, there are major benefits to Integrated Cost Management. One of which is lowering of overall costs throughout the product life cycle.

Integrated Cost Management can facilitate a steady decrease in costs all the way to discontinuance. In fact, it can result in an annual cost reduction of about 17% during manufacturing, savings that exceed 30$%, and a designed-in cost of below 70%.

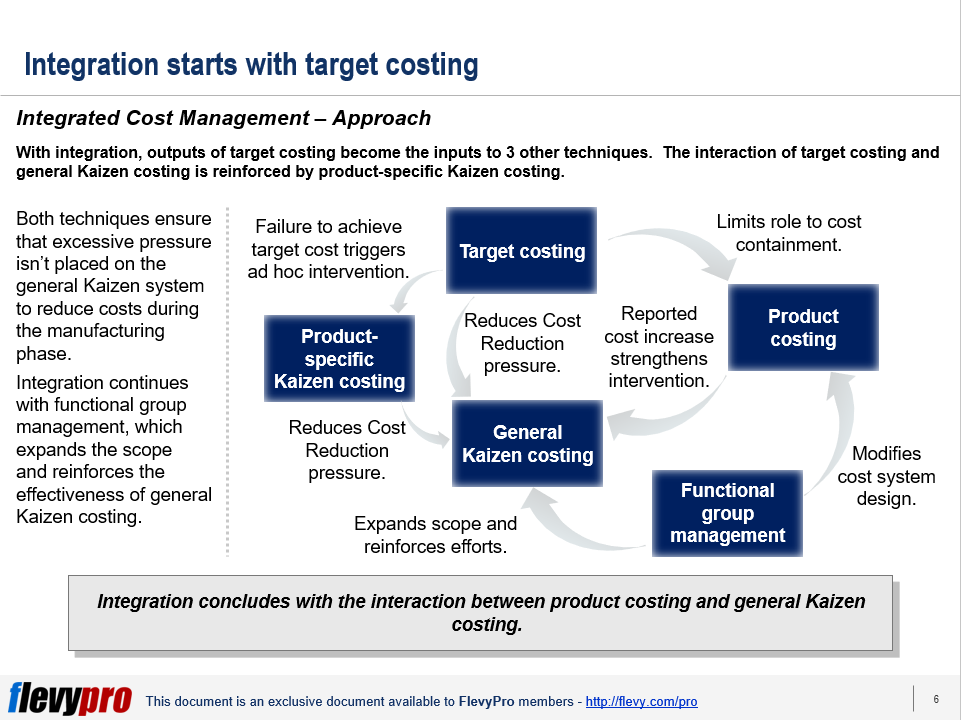

Achieving this requires an understanding of the Integrated Cost Management Approach.

The Integrated Cost Management Approach focuses on the integration of cost management techniques which can lead to higher levels of cost reduction and superior overall performance.

The Integrated Cost Management Approach takes into consideration 5 Cost Management Strategies.

The 5 Cost Management Strategies enable organizations to better manage costs throughout the product life cycle, with just one (1) technique taking place during the product design and the rest during manufacturing.

The application of the 5 Cost Management strategies has its key takeaways. These can be used as a guidepost in its application and a model of general concepts that organizations may consider.

One key takeaway is significant savings can still be achieved with short life cycle products and aggressive cost management focused on product design. Taking to note this key takeaway, we have to consider that as the length of the manufacturing phase of the product’s life cycle increases, the opportunity for cost reduction increases. Further, there is a need to explore the value of integrating multiple cost management during manufacturing.

Interested in gaining more understanding of Integrated Cost Management? You can learn more and download an editable PowerPoint about Integrated Cost Management here on the Flevy documents marketplace.

Are you a management consultant?

You can download this and hundreds of other consulting frameworks and consulting training guides from the FlevyPro library.